Alternative Proteins: The Good, Bad & Ugly

“If slaughterhouses had glass walls, everyone would be vegetarian.”

Paul McCartney — singer, songwriter, and musician

It all started with a dream, or more precisely, dreams. Consumers envisioned a healthier lifestyle fuelled by more plant-based foods (without sacrificing taste, of course). Food producers, animal rights activists and scientists thought they had found the holy grail using a new approach that would address consumer health, animal welfare, and profits. Investors were seduced by the prospect of huge returns by funding the next big thing and doing some good along way.

Creating fundamental change requires significant time and a sustained effort; the alternative protein sector is no different. As we close the first chapter of its development, we find some areas have surpassed all expectations, while others are developing, and the remainder are an ongoing source of pain and uncertainty. This led us to consider the good, bad, and ugly of the alternative protein sector.

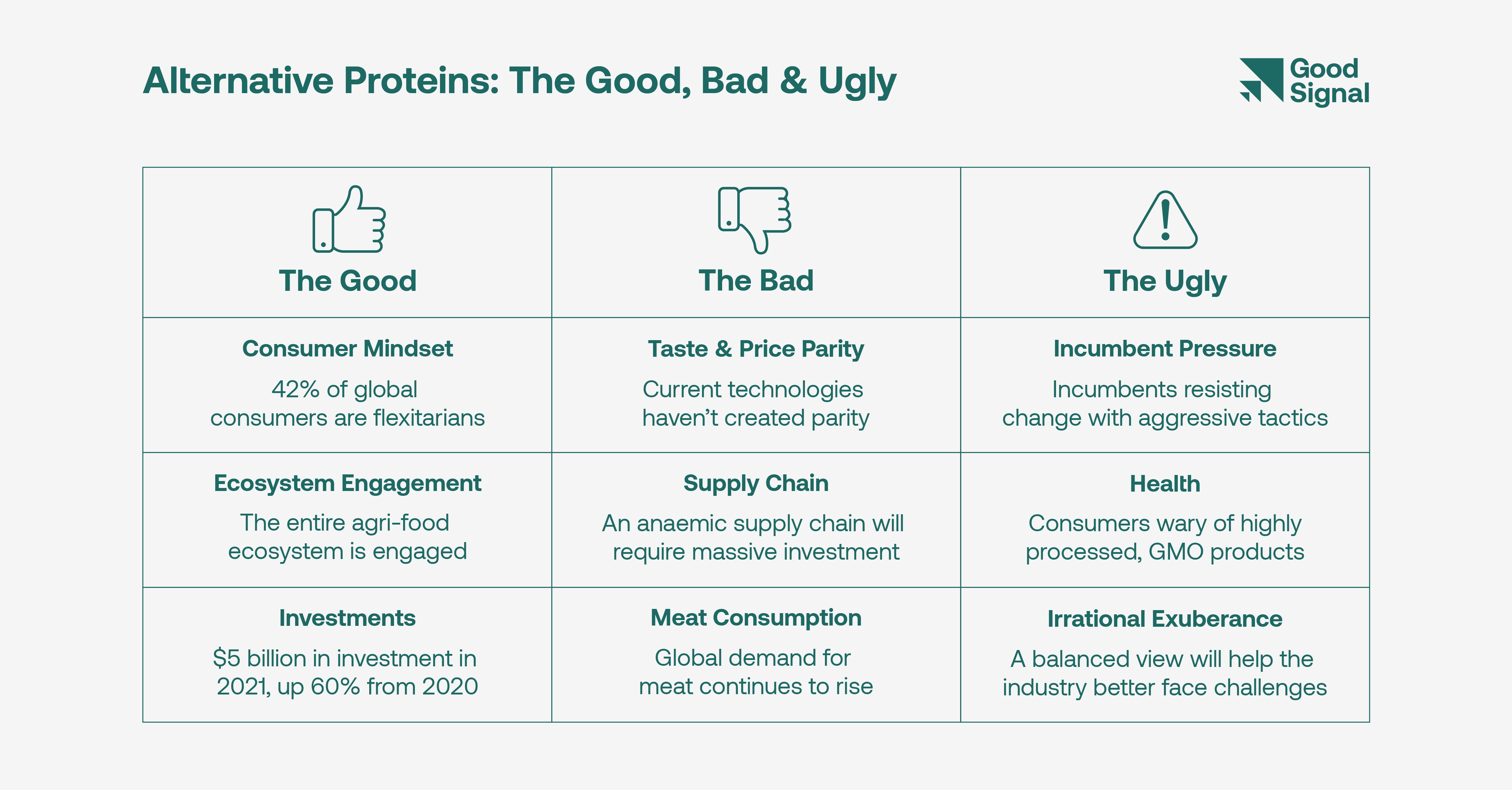

The Good

The consumer mindset has shifted. The ‘flexitarian’ movement is fully underway. Globally, 42%1 of consumers call themselves flexitarians. In the United States, the most advanced market for such products, the number rises to 47%.2 In the millennial population (or younger), flexitarians comprise a majority of the segment. Whether it’s health, animal welfare, or sustainability, an increasing number of consumers love the idea of eating well and doing good. As the quality of alternative protein products rises, they capture the hearts and minds of an ever-greater number of consumers. Plant-based milk is on its way to becoming mainstream, while Impossible and Beyond have become global brands with others following in their footsteps. If you’re a trendy restaurant in a global city, then you have likely considered putting Impossible on the menu. Oatly has found its way into cafes big and small, while visionary ones such as Nestle-owned Blue Bottle have made oat milk the default choice of milk (that is, you must explicitly ask for cow’s milk in your latte). Imagine that.

The development of a new industry requires broad ecosystem engagement to create rapid growth. This includes governments, academia, incumbents, startups, infrastructure players, investors, and consumers. The alternative protein sector is fortunate to see this happen in spades. Further, Covid highlighted the issue of food security, which alternative proteins are well positioned to address due to their reduced resource usage and potential for localised production. This has motivated governments to explore this area. This fits well with Singapore’s ‘30-by-30’ initiative to produce 30% of its nutrition locally by 2030. Alternative proteins are one of three key initiatives to reach this goal for the island-state (along with vertical farming and aquaculture). China has referenced alternative proteins as part of its 14th five-year plan.3 Academic institutions have started research and classes, fuelled by student demand and research grants. Every major meat producer has a plant-based meat brand, and most are investors in startups in the sector. Food producers are busy launching their own products and ramping output. While only Singapore and the Netherlands have approved selected use cases of cultivated meat, U.S. regulatory approval is widely expected in the next 1-2 years, which will be a watershed moment for the sector.

Investors pumped US$5 billion into the sector in 2021, up 60% from 2020. While funding for plant-based startups remained steady, fermentation and cultivated technologies saw a huge spike, each approximately tripling in size and approaching plant-based in their respective investment levels. Taken together, the sector received 45% of its total funding since inception in 2021 alone, a staggering number. Along the way, the sector has globalised. Non-U.S. companies received 33% of total funding for the sector, reflecting a steady increase over the past decade. Globalisation is even more pronounced by technology stack. U.S.-based fermentation companies received only 58% of total funding, and cultivated companies in the region received just 51% as Israel has become a hub for cultivated meat startups.4 Even in a challenging economic environment, we will see increasing scale and ubiquity.

The Bad

In the food industry, there is a saying: ‘taste is king; price is queen’. In 30 years, when our food system will be transformed by technology, we believe these words will still ring true. The holy grail for the sector is to achieve taste and price parity with animal products, which is still many years away. Plant-based foods, for all their hype, have been unable to deliver. The plant-based approach typically takes an ingredient, like soy or peas, and disposes much of it, using a fully chemical process to create a concentrate or isolate. Then, gums and emulsifiers are added along with a host of other ingredients to mimic products with different functional characteristics, all of which must be done at price parity. It’s no wonder the approach hasn’t been successful. Today, consumers are left wondering why they are paying more for a product that doesn’t taste as good as its conventional counterpart. However, fermentation and cultivated technologies, which are rapidly coming online, offer favourable characteristics that complement plant-based technologies.

A major hurdle to reaching taste and price parity is the anaemic supply chain of the sector. The plant-based movement was built largely on a limited number of ingredients – soy, peas, oats, and pulses – produced using legacy processes and infrastructure. We have only scratched the surface of plant-based ingredients and haven’t yet honed processes to effectively utilise them. As the sector globalises, unique ingredients will emerge for each region, which not only cater to local taste profiles but can also be sourced more easily and economically. For the sector to thrive, it must develop supply chains across each technology stack – plant-based, fermentation and cultivated – and create processes and infrastructure to match. A recent Good Food Institute (GFI) report concluded that $27 billion in capital expenditures by 2030 would be required for the plant-based segment alone, which assumed a modest 6% market share of animal products. An additional $17 billion in annual expenditure would be required to utilise this infrastructure.5 This is to say nothing about the infrastructure and operating capital for the fermentation and cultivated segments, which are each likely to be larger.

Despite greater awareness about the significant impact of animal agriculture products, meat consumption continues to grow globally. The population of our planet will reach 9.7 billion people in 2050.6 Greater affluence across the world also fuels the demand for animal products. As incomes rise, people eat more meats, oils, sweeteners, fruits, and vegetables, suggesting that global demand for animal-based foods will increase faster than population growth.7 As a result, overall meat consumption is on track to grow 73% by mid-century.8 This will require consumers to change their behaviour to opt for alternative proteins (an uphill battle) even as production matches increased demand.

The Ugly

Incumbent pressure continues, as giants of the food system fight to preserve their empires. At surface level, this is no different from incumbents in any industry facing disruption. However, the techniques being utilised reflect an aggressive approach designed to stifle innovation and slow the pace of change. A key battleground is labelling. In the U.S., an active lobby persists to prevent alternative proteins from being called meat, seafood, dairy, or eggs. Indications are that the animal agriculture lobby will be largely unsuccessful in curbing labelling guidelines with the recent win by Miyoko’s plant-based butter providing an early precedent. Globally, the battles for labelling are ongoing, such as proposed restrictions in Europe for dairy products such as milk, butter, and cheese. Other questionable techniques include misinformation campaigns, such as those purported by the largest dairy cooperative of India, which is taking out full page ads in mainstream publications to spread questionable facts and information, relying on the age-old adage that if you have a loud enough megaphone, people will listen. In the U.S., meat producing states have implemented ‘Ag-gag’ laws that criminalise even investigating the practices of factory farming. The industry also benefits from a price advantage derived from aggressive lobbying. Far from paying for its impact on climate change, the animal agriculture industry has received subsidies in the name of food security and rural employment while largely avoiding the blame. Since the meat industry isn’t paying for its externalities, this creates artificial pricing pressure on new products that must compete with it.

Health remains a major driver of consumer adoption of alternative proteins even as products go to ever-greater lengths to achieve taste and price parity. Today when consumers purchase meat products, they often see a single ingredient (e.g., ground beef). Unfortunately, this masks the contaminants, antibiotics and hormones that may have been part of the production process before the product arrives at the supermarket. When a consumer purchases salmon, for example, the ingredient label says nothing about the mercury or microplastics that may be present inside. Alternative protein products are afforded no such luxury. Beyond Burger utilises 18 ingredients while Impossible Burger utilises 21 ingredients, all of which are fully visible to the consumer on the ingredient label. As product ingredient decks swell with items most can’t pronounce, much less understand, coupled with the presence of controversial technologies such as GMOs, consumers are left wondering whether they are moving from processed to ‘hyper-processed’ products. According to Mintel, six out of ten consumers would eat more meat alternatives if they were less processed. Shouldn’t an industry with a health and sustainability imperative create products that give consumers confidence around those goals? In this respect, the industry has a long way to go.

The term ‘irrational exuberance’ was first used by then-U.S. Federal Reserve Bank Chairman Alan Greenspan in 1996 to describe investor enthusiasm that drives asset prices higher than fundamentals justify. We find ourselves in a situation where the industry is so busy applauding its own achievements that little attention is paid by most to the bona fide risks that surround it. Valuations have climbed to stratospheric levels traditionally seen in sectors such as software which see far higher margins, significantly less friction to scale, and face limited regulatory hurdles. The frenzied pace of investment has created an environment where valuations have soared, company fundamentals aren’t prioritised, and scientific diligence takes a back seat. The recent market meltdown will leave many companies with valuations too high to raise capital and burn rates that may not get them through the downturn. As the stocks of public entities like Beyond Meat and Oatly come back down to earth, the result is disappointment and skepticism that drags down the rest of the sector with it. Even Impossible Foods, the top brand in the sector, is seeing its stock trade lower in secondary markets than its valuation in its most recent round. Unless the sector focuses on fundamentals, there is a real chance that it won’t see long term growth. We cannot afford for this to happen.

The Road Ahead

This sector must succeed. We’ll have a protein shortage by 2050 if we keep doing what we’ve been doing. Innovation, fuelled by technological advancement, is the most promising path to a brighter future. It enables us to do more with our existing resources, to uncover possibilities that don’t exist in our world today. In the technology industry, Moore’s Law enabled a revolution and led to the rise of the computing age over the past 50 years. We are seeing a similar trajectory with biotechnology, as evidenced by the plummeting cost of sequencing the human genome. The sector is emerging but requires sustained effort. Just as a plane consumes the most energy during take-off, the industry must marshal resources to rapidly propel the sector forward. When expending its maximum energy upon takeoff, an airplane has the least energy to waste. Similarly, innovators in the sector must deliver upon promises with a laser-like focus. As much work as we have to do, we are off to a promising start.

Euromonitor

Sprouts Farmers Market & One Poll

China’s Ministry of Agriculture & Rural Affairs

Good Food Institute

Good Food Institute

United Nations

Wikipedia

Food and Agriculture Organization