Market Map: A Snapshot of the Alternative Protein Sector

“In 30 years, it is unlikely animals will need to be killed for food anymore.”

Sir Richard Branson, Founder — Virgin Group

When the Internet commercialised in the early 1990s, it was the start of a 30-year journey that has led us to where we are today. The brands, applications and services that permeate our lives – Google, Amazon, Facebook, Netflix, Airbnb – didn’t exist then. The mobile phones that have become our constant companions weren’t a part of our lives either. It’s hard to imagine our lives without them today.

Our food system is undergoing a transformation that few of us will recognise in 2050. Three major trends are driving the change. First, consumers are shifting their mindset. Increasingly, people want to eat healthier, which has sparked a trend toward plant-based foods. Second, food production is utilising not just food science and ingredients, but biotechnology and molecules. Make no mistake, this is as fundamental a change as the transistor was for the computing age, which ushered in a new era leading to modern computing platforms. We have already started to create foods with version numbers, just like software. Finally, a sustainability imperative is upon us. We are heading toward a planet with 10 billion people, with a substantially more affluent population. The result will be a greater demand for animal products. We will be unable to meet this demand unless we do something radically different. In addition to food security, we are facing limits to our natural resources which are negatively impacting the planet.

Animal agriculture is a highly inefficient method to produce food. For every calorie of food we produce, it takes between 9 to 25 calories of input.1 As a result, we currently utilise 77% of farmland to produce just 18% of our food.2 Alternative proteins offer a better path because they utilise up to 90% less energy3 as well as 99% less land and water4 to produce similar products. While resource usage varies with each process and technology platform, it is clear alternative proteins provide significant advantages in resource utilisation. Admittedly, they are early in their development, much as the Internet was thirty years ago. The skeptics then would have found their brethren today. This is not to say there aren’t risks and challenges, but making sustainable change is never easy.

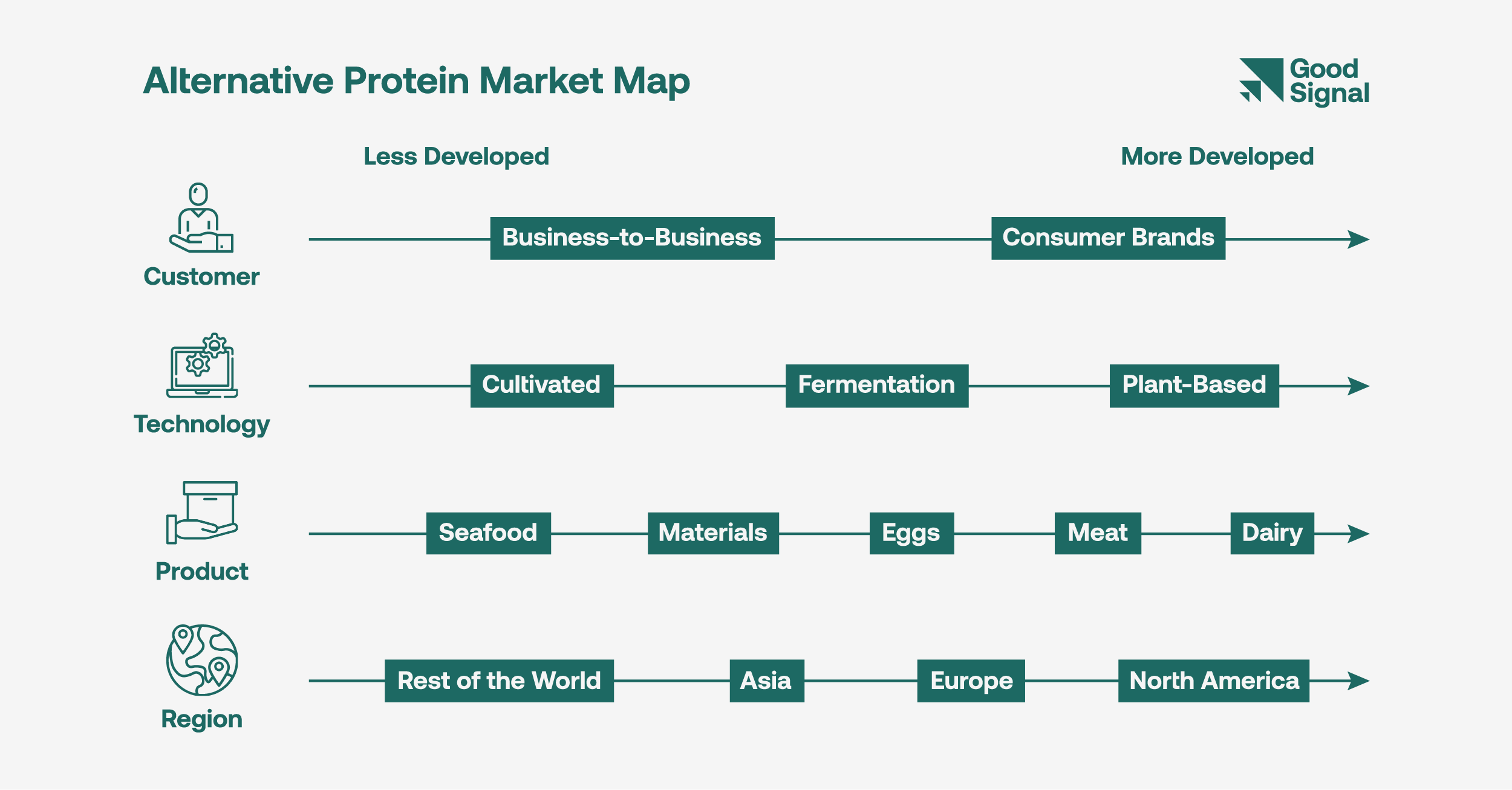

The alternative protein “market map” below provides a snapshot of the current state of the alternative protein industry across four key vectors: (1) Customer; (2) Technology; (3) Product; and (4) Region, showing their relative development.

The Customer Vector

Consumers have experienced the alternative protein sector through top brands such as Impossible, Beyond and Oatly. It is truly remarkable that they are collectively available in 100,000+ retail outlets. Their innovative products and global reach have opened consumers’ minds to new possibilities. However, just as we saw with the Internet, this first wave of companies is largely vertically integrated, creating and leveraging internal processes and customised equipment. So, even as Impossible Foods, Beyond Meat and Oatly built innovative products and established substantial brand recognition, they had to do so using a relatively limited set of available ingredients (e.g., soy, peas, oats, pulses) while relying on legacy processes and equipment. This led to years of R&D fuelled by hundreds of millions of dollars of investment to create their products using specialised processes and ingredients, for example, heme, to provide the “meatiness” of meat.

The collective market cap of the top three consumer brands, following the recent market beating, is approximately $10 billion. In contrast, the top three privately held ingredient startups focused on the supply chain (Perfect Day, The EVERY Company, Motif FoodWorks), are collectively worth about a quarter5 of that, and are in relatively early stages of commercialisation. It is exciting to envision the acceleration of the sector once there is a formidable supply chain. We need this to happen urgently if the sector is to thrive. Over the past year, we have seen innovation across the supply chain of each of the major technology stacks – plant-based, fermentation and cultivated – with multiple companies tackling highly specific challenges faced by the sector.

The Technology Vector

The allure of plant-based foods has helped bring alternative proteins closer to the mainstream. Plant-based meat and dairy offer “flexitarians” an opportunity to have their cake and eat it too. They are eating plants that taste like meat, well almost. But almost isn’t good enough, and despite the progress made with Impossible Burger 2.0 and Beyond Burger 3.0, it’s clear we have a long way to go. Bridging the taste and texture gap remains highly challenging and may never be possible with plant-based technologies alone.

What makes the potential of alternative proteins especially compelling is that there are multiple technology stacks at work. As fermentation and cultivated technologies come online, the quality of products will rise dramatically. While plants provide desirable nutritional profiles, fermentation brings not only the potential to design precision proteins, but also to create biomass using a variety of microbes. Cultivated meat, in a sense, is the holy grail, as it is real meat without the antibiotics, hormones or contaminants, and most importantly without the animals. But it isn’t what happens when we choose one technology stack or the other, but rather when we put them together that is compelling. ‘Hybrid’ products enable the creation of foods which integrate nutrition from plants, proteins via fermentation and taste and texture from cultivated meat. Beyond mimicking animal products, the potential to create new, highly unique products, all of which cater to consumers’ desire for animal products, is unlimited.

The Product Vector

The U.S. market, which leads the world in consumer adoption of alternative proteins, has seen plant-based milk take 15% market share in the overall milk market. While Oatly and similar brands aren’t a true substitute for milk in taste and texture, their distinct taste, nutrition, and sustainability benefits have won over consumers, who increasingly see these products as a unique category. The comparable share for total plant-based retail meat in the U.S. is just 1.4%.6 Alternative seafood and eggs lag further behind with a limited set of offerings today, along with materials like leather.

This is evident in the market caps of companies in the sector, where plant-based milk has three unicorns (Oatly, Califia Farms, NotCo), compared to two in plant-based meat (Impossible Foods, Beyond Meat), all of which are seeing significant consumer adoption, while the egg category has only one (Eat Just). Seafood has comparably limited consumer adoption and investment, though this is changing quickly. A notable exception is the strong investment in biomaterials with Modern Meadow, Spiber and Bolt Threads all raising significant capital, but none has an established brand name or widespread adoption to date.

The Region Vector

North America continues to retain its dominance in the alternative protein sector, both in consumption and production. U.S. companies are leveraging a deep talent base along with a well-established ecosystem of innovation. Of the top 10 highest market cap companies in the sector, eight are in North America (the other two are in Sweden and Chile)7. Of course, there are incumbents in the space such as Quorn, but the new breed of companies is innovating significantly on the technology platforms and quickly establishing global brand recognition.

We are also seeing the initial signs of specialisation. Israel is fast becoming a hub for cultivated meat. Singapore is establishing an advanced regulatory pathway along with a favourable environment for both R&D and manufacturing. Agrarian-based economies will undoubtedly establish footholds in the supply chain. The U.S. is leading innovation, like it has in many other industries. Further, companies increasingly require a multinational presence as they look to address their needs across four areas: (i) supply chain e.g., input materials; (ii) research and development; (iii) manufacturing and scale-up; and (iv) distribution. We believe we will see specialisation across and within these four areas over time. Consumer demand will drive further specialisation. Today, China consumes half the world’s pork8, Asia consumes 70% of seafood9, and India is the largest consumer and producer of dairy.10 Undoubtedly, as the alternative protein sector moves from approximately $30 billion today to $1-2 trillion by 2050, companies in these regions will strive to tailor their products to meet consumer needs.

A New Hope

We are at the end of the first chapter of alternative proteins, during which we have experienced only the beginning of this transformation. The industry has innovated in the areas of ground meat substitutes and plant-based milk, creating two significant public companies – Beyond Meat (NASDAQ: BYND) and Oatly (NASDAQ: OTLY) – and the most valuable company in the sector, Impossible Foods, valued over $5 billion. The next chapter will be considerably more active.

It’s virtually impossible to get a glimpse of fundamental innovation, even when it’s right around the corner. Whether it was electricity, the car, the airplane, or the transistor, people may have envisioned some version of this invention for a long time, but even a short time before these inventions changed our lives, most people weren’t banking on their benefits in their day-to-day living. We can’t envision what’s coming any more than we could envision the iPhone one year before it arrived. What we know is that we’re at the beginning of a fundamental change to our food system. Technology is like a juggernaut that disrupts one industry after another. We have seen this happen with energy, transportation, and healthcare. Our food system is next.

Disruptions are challenging even for those that choose to adopt them, and especially for those who are left behind. We must make every effort to include the various players in the food ecosystem – governments, food manufacturers, retailers, farmers, workers, consumers, and investors – because this will both accelerate change and create a better outcome for everyone. There is no technological shift in history without skeptics, or with a guaranteed outcome. While the adoption of these technologies is far from certain, it’s encouraging to see participation from all the major ecosystem players. In 1996, Jim Barksdale, then the CEO of Netscape, a dominant company in the Internet’s early days, said that “the Internet is the printing press of the technology era.” The technology stacks being developed today will similarly become the foundation of the next generation of our food system and help sustain generations to come.

Yale - Center of Business and the Environment

Our World in Data

The American Journal of Clinical Nutrition

Good Food Institute

PitchBook

Good Food Institute

PitchBook; public market data

The Washington Post

Nikkei Asia

Dairy Industries International