Triggering the Transformation to Alternative Proteins

“Transformation is a journey without a final destination.”

– Marilyn Ferguson

Asia was once a pioneer in technology development. Many important ancient inventions such as gunpowder, paper, silk, and printed press which we still utilise in modernised or improved forms were created in Asia. Although it accounted for approximately 60% of global output by the 1700s, its share had fallen to below 15% by 19501. If history has shown us one thing, it is that technological progress requires the ability to manage and adapt to constant change. By preempting disruption, we can not only be better prepared to embrace it, but also leverage it to further our progress. Our food system is at the cusp of a major disruption. By mid-century, alternative proteins are going to fundamentally transform the way we consume food. Asia will be the major market for many alternative protein product categories and thus, startups in the region are well placed to meet the requirements of the local populations if they can rise to the challenge.

The initial phase of the alternative protein adoption has been a bumpy ride – over the past decade, the industry has had to educate consumers, bear significant R&D costs, face an aggressive incumbent lobby, deal with a pandemic, and navigate a sluggish economy. There has been much focus on the future adoption of alternative proteins and the market share it will command by mid-century. A recent article by Synthesis Capital aptly summarised varied scenarios for alternative protein adoption along with their view around adoption via an S-curve. We found the analysis compelling. With an S-curve that outlines the shape of the transformation, we now look to understand what lies underneath with a focus on products and regions that will lead this shift.

Adoption will ultimately be driven by consumers’ willingness to reduce or substitute animal products. Their dietary preferences are in turn based on a wide variety of personal, social, cultural, and environmental factors. Early indications have emerged from both purchasing patterns as well as surveys about consumer preferences, though most consumers don’t yet know what future offerings, such as cultivated meat, may look or taste like. It is interesting to note that while Western markets such as the U.S. and Europe have taken an early lead in consumer adoption, the interest in plant-based products is higher in eastern markets such as China and India. According to recent surveys, 95% of Indian and Chinese consumers were somewhat to extremely likely to buy plant-based products, while this number stands at approximately 75% for U.S. and 86% for European consumers2. Using data from FAO and OECD, current sales figures across different markets, and consumer acceptance surveys, we explore what the future might look like for alternative protein adoption across products and regions.

A Product Transformation

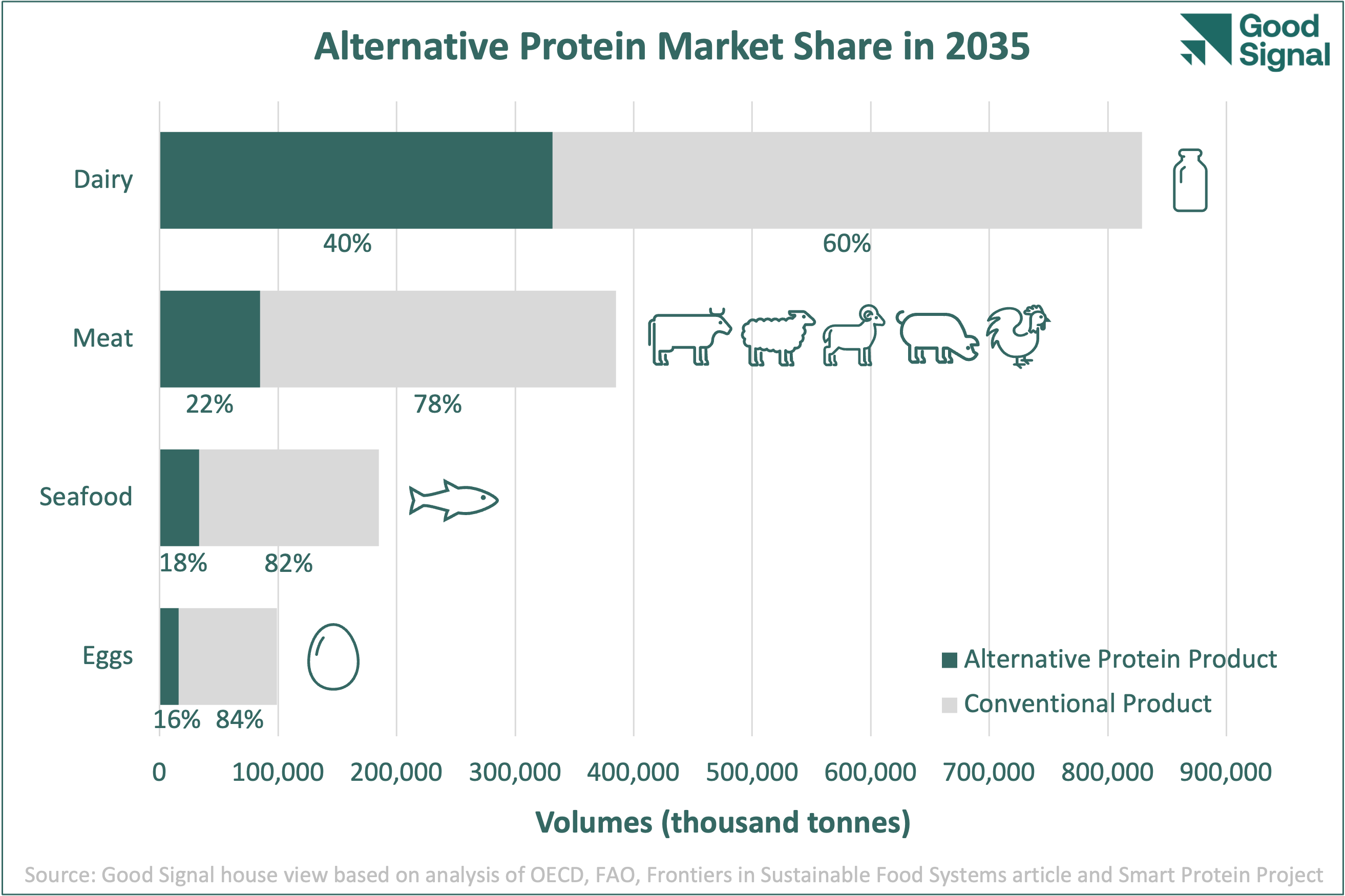

The current adoption of alternative proteins varies vastly across the different product categories. In the leading market, the U.S., alternative milk commands the highest percentage market share compared to all other product categories at 16%. Meat, in contrast, is still at a paltry 1.4% with eggs trailing further at 0.6% and alternative seafood the laggard at 0.1%3. According to our analysis, global adoption in 2035 will look rather different.

Meat: The global meat market will rise to 385 million tonnes by 2035. Alternative meat will command a market share of 22% by then. Chicken will see the highest adoption levels of substitute products by volume given its broad footprint in global consumption. Pork will see similar levels given the high level of consumer interest in China, which consumes half the world’s supply. The U.S. will drive the adoption of alternative beef, given its head start with consumer adoption. While mutton and goat are the preferred meat in regions such as the Middle East and India, they will take a longer time period to traverse the S-curve. Two factors will drive this transformation. First, as cultivated meat comes to the market with technological innovation, larger manufacturing facilities and global regulatory approval, it will give consumers products that are indistinguishable in taste and texture. Second, the drive for superior products will combine all available technology stacks – plant-based, fermentation, and cultivated – to create hybrid products that not only deliver great taste and texture but also superior nutrition. Although most of the innovation in alternative meats so far has been focused on beef and chicken which have the highest number of startups, we are increasingly seeing more companies working on other species. Ultimately, for the alternative meat market to reach an inflection point, we will need improvements across all the four key vectors: taste, texture, price, and nutrition.

Eggs: We project a 16% market share for alternative eggs by 2035. Innovation in this category has been focused more on the ingredients space or on liquid eggs. Replicating solid consumable egg formats (e.g. whole eggs) remains a challenge that may impede consumer adoption. Replicating the whole egg is especially difficult because consumers are looking for an experience (i.e., breaking the shell) that requires considerable R&D. To make matters worse, startups need to deliver at the price point of a highly commoditised product. As a result, this sector will initially see greater traction with B2B applications, targeting markets such as baked goods, confectionary, and other adjacent markets. It is promising, however, that we can rely on innovation from the plant-based and fermentation technology stacks, which are seeing significant traction today, to deliver these products.

Seafood: After a slow start due to a lack of attention from both startups and investors, we expect the market share for seafood to rise significantly to 18% by 2035. Plant-based seafood remains a nascent category because a fishy taste and texture have been challenging to replicate with plant-based ingredients compared to meat. Seafood will see a unique adoption curve since Asia consumes approximately 60%4 of the world’s seafood with 70%5 of it eaten outside the home. The sector benefits from higher pricing for selected categories, which can aid market entry. While a number of promising startups are working on plant-based seafood alternatives, we have seen outsized funding rounds for cultivated seafood startups such as BlueNalu and Wildtype. As a result, it is exciting to chart a future where we see a wide range of products in this segment, including hybrid offerings leveraging various technology stacks.

Dairy: The ascent of plant-based dairy alternatives has been unprecedented with a 12.5% share of the total dairy market6. The adoption has largely been driven by alternative milk but also includes cheese, butter, ice cream, yogurt, and other dairy offerings. The projected 40% share that alternative dairy will command by 2035 will serve to do nothing less than upend the industry. Alternative dairy commands a 22% market share in Asia Pacific, where a majority of the consumers are unable to process dairy7 (an estimated 80% adults in Asia Pacific are lactose intolerant). However, alternative dairy is still significant in markets like the U.S. and Europe with 9% and 6% share, respectively8. While China dominates the alternative milk market because of its long-standing tradition of consuming soy milk, Europe is the leading region for alternative cheese adoption9. Today, the market is comprised mainly of plant-based alternatives, which have surprisingly carved out a category of their own. Unlike blind taste tests for meat products, no one is doing a blind taste test comparing plant-based milks to their local milk brand. Consumers don’t expect Oatly, for example, to mimic the taste of milk; they simply see it as an alternative. To some extent, this is a shortcoming of plant-based technologies, so it is especially remarkable to see consumer adoption at this level. What will happen when alternatives are indistinguishable from milk and cheese, yet offer better nutrition without the issue of lactose intolerance? As precision fermentation and cultivated technologies come online for this category, consumers will see an explosion in alternatives available to them. With improved functionality, these products will subsequently tackle downstream milk products, which will have ripple effects we can scarcely imagine today. Cultivated technology is likely best suited to replicate complete milk formulation, but for B2B applications such as casein proteins for cheese production, we see precision fermentation as the preferred technology.

As far as we have come in this industry, much of the innovation remains ahead of us. During this initial phase, alternative protein companies have been vertically integrated, doing everything in-house. The product transformation, however, will be turbocharged by startups with deep specialisation, and each technology stack finding its niche across the various product categories.

A Regional Transformation

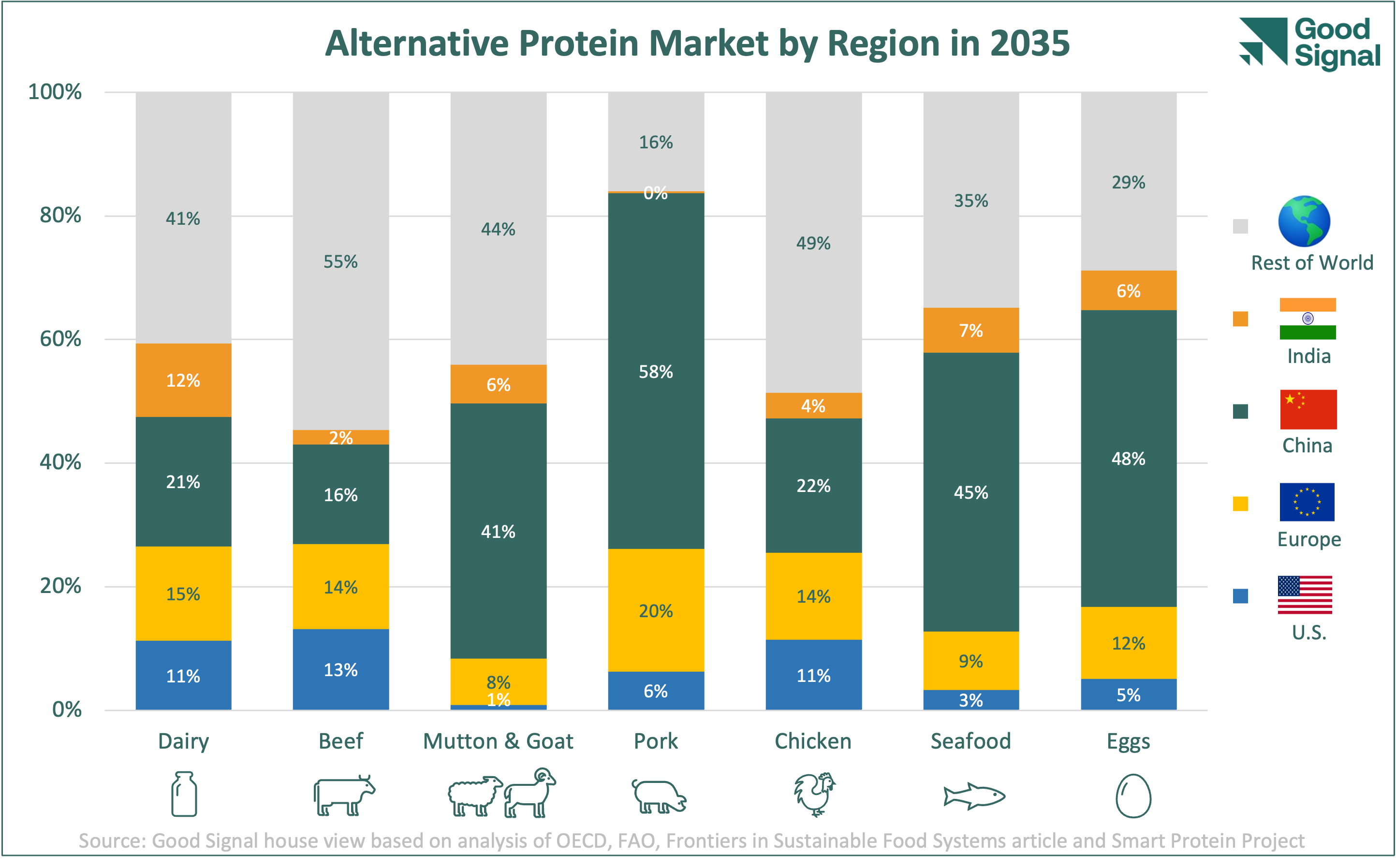

When it comes to consumption of animal products, the standouts are the U.S., Europe, China, and India. While the latter ranks low in meat consumption, its consumption of milk is outsized. Further, India’s sheer size and the projected increase in meat consumption10 make it worthy of a closer look. Let’s explore the adoption of the various product categories across these regions.

United States: The U.S. is expected to be a key market for three alternative protein products – beef, chicken, and dairy. It has been the leader in the development of the alternative protein ecosystem both for both supply (number of startups) and demand (number of consumers). With well under 5% of the world’s population11, we expect it will command a 13% share for alternative beef and 11% for both alternative chicken and dairy. The recent ‘no objections letter’ from the Food and Drug Administration to Upside Foods for cultivated meat will further advance innovation in the region. Consumer focus on climate impact, sustainability, health, a desire for great taste, and competitive pricing will continue to drive adoption.

Europe: The European landscape has contrasting effects due to a higher focus on sustainability than other regions but a more stringent regulatory environment. Europe is expected to be a significant market for alternative dairy, commanding 15% of global share. In addition, it is expected to be 14% of the global alternative meat market for beef and chicken and 12% for egg. Environmental concerns among European consumers rate highly and are driving adoption with 60% of consumers in France and Germany, 66% in Spain, and 71% in Italy saying alternatives to conventional meat are necessary12. Though cultivated meat faces a more drawn-out regulatory process relative to other regions, consumers across Europe want governments to support it; 38% of consumers in France, as well as a majority in Germany, Italy, and Spain, believe it would have a positive environmental impact13.

China: China is poised for a sea change from an alternative protein standpoint by 2035. It is predicted to command over 40% market share across four product categories: pork, mutton & goat, seafood, and eggs. In addition, it will be the leading consumer of alternative beef, dairy and chicken. Given Asia’s long history with plant-based alternatives such as soy, the benchmarks for the industry will remain high, but consumer willingness to try these alternatives provides hope. The primary driver for Chinese consumers to switch to alternative proteins are health benefits while sustainability and ethical concerns rate lower14. The industry must focus on smart marketing with effective messaging to position the new generation of alternative proteins as distinct from the mock meat products that consumers in the region are so accustomed to. In addition, Chinese consumers will likely demand pricing that is in line with mock meat products they are purchasing today, which creates an additional challenge.

India: India has a unique relationship with dairy. In addition to being the largest producer and consumer of milk in the world15, the Hindu religion holds the cow sacred, placing dairy in a special category. Its leading dairy cooperative remains intertwined with the livelihoods of millions of smallholder farmers. Alternative meat consumption is expected to increase immensely in India along with meat consumption overall. However, alternative dairy remains the most interesting category, owing to the sheer volume of dairy consumption and the complex interplay between a large lactose intolerant population, India’s history with dairy, and an aggressive incumbent dairy producer. According to Pew Research, four-in-ten Indians identify as vegetarians, and an equivalent number want to limit meat in their diet. As a result, meat alternatives are currently a niche segment in India, supported primarily by millennial consumers in major cities who are open to exploring new products. The population also remains highly price sensitive and will demand products that are affordable or at price parity with conventional alternatives.

Today, the West leads in alternative protein innovation driven by the U.S., while Asia offers the most advanced regulatory pathway, led by Singapore. In addition, Israel has been a standout in cultivated meat. For every region, a concentrated effort is required to develop each category with innovation across the value chain, spanning ingredients, processing, supply chain, and distribution. Regulatory approval in any new region holds the key to turbocharging local startup innovation and setting the stage for wider consumer trials, in-turn driving consumer adoption and product innovation.

The Opportunity Ahead

As we look to 2035, two observations stand out. First, alternative proteins are set to play a meaningful role in our food system. With approximately 30% of the market share by volume, they will be well on the way to traversing the S-Curve, culminating in becoming staple foods for the mainstream consumer. Second, Asia will play a significant role in the transformation, leading the charge with over 50% share of alternatives in at least four product categories (eggs, seafood, pork, and mutton & goat), and over 25% share in two others (dairy and chicken). Asia will consume 70% of all alternative seafood by 2035. To date, much of the innovation in the alternative protein industry has been focused on products that are appealing to western consumers, such as burgers and nuggets. To get the Asian population excited about alternative proteins, product and technology innovation must focus on local products such as dumplings and sushi. Innovations need to transcend texturisation of minced meat to formulate whole cuts and clean label products. To do so, the industry will need to expand its ingredient toolkit by addressing the anaemic supply chain. Asia, as a predominantly agrarian economy, is perfectly suited to enable production of local ingredients that are nutritious, sustainable, and provide food security.

We stand at the precipice of unprecedented change in our food system. While the size and shape of the next phase is unclear, there are opportunities abound to make an impact and create a better future. Whether it’s to improve the supply chain, utilise new technologies such as cultivated meat and molecular farming, or create new products that serve local tastes, we will see a new generation of companies emerge alongside the work incumbents are doing to leverage this opportunity. To get there, we will also need engagement from governments, researchers, entrepreneurs, and investors, who each play an important role. Along the way, we will impact climate change, human health, animal welfare and sustainability. There are exciting times ahead.

Asian Development Bank, Asia 2050: Realising the Asian Century

Frontiers in Sustainable Food Systems: A Survey of Consumer Perceptions of Plant-Based and Clean Meat in the USA, India, and China

Good Food Institute (GFI)

Hapres Journal of Sustainability Research: Drivers of Seafood Consumption at Different Geographical Scales

The Counter

Citi Research, Euromonitor

Citi Research, Euromonitor

Citi Research, Euromonitor

Maximize Market Research (MMR), Vegan Cheese Market Global Industry Analysis

Bennett (1941), International Contrasts in Food Consumption

Worldometer, U.S. Population

GFI Europe

GFI Europe

Fi Global, Plant-based Market in China

Dairy Industries International