The Road to Addiction

“The purpose of a business is to create a customer who creates customers.”

– Shiv Singh

ARTICLE SUMMARY

The world’s best companies don’t just have loyal customers; they have addicts, who consume their products at high velocity. In the alternative protein sector, the quintessential example is the consumption of plant-based milk by younger consumers. Millennials and Gen Z are early adopters who consume the product regularly due to their shared values and fresh perspective on what should constitute their diet. There are numerous benefits to targeting them over other consumers or ‘flexitarians’ as they have rising purchasing power and a long consumption runway. As the industry looks to mainstream adoption, the best strategy would be to target younger consumers by creating products, developing messaging, and utilizing sales channels specifically geared to win them. When it comes to gaining a 30%+ share in the animal products market, it’s not just about winning 3 out of 10 consumers; it’s about which 3.

For a moment, consider the products you cannot live without. People cite some of the world’s most iconic products, including Google, Coca-Cola, and the iPhone, to name a few. While radically different, they share one key characteristic: they create addicts – large numbers of them. Google couldn’t build a great business if its most active users only visited the site once in a while. Nor would someone pay over US$1,000 for a new version of an iPhone every year if they only used it periodically. Creating loyal (or better yet, addicted) users, which form the core of any significant brand’s most valuable user base, lies at the heart of product design.

A loyal customer displays repeat purchase behavior. An addict does so at high velocity. This is essential — a food-related business would have to win 30 loyal customers that consume a product monthly, compared to just 1 addict that consumes it daily. The dividends of repeat purchase behavior are well understood, as customer retention increases sales per customer while reducing customer acquisition costs. 67% of returning customers spend more in their third year of buying from a business than in their first six months. Average customer acquisition costs have increased from $9 to $29 over the last decade. As a result, by increasing the customer retention rate by just 5%, companies can increase profits by 25% to 95%1. A great business doesn’t just need customers; it needs addicts who love the product, consume it at high velocity, and spread its gospel to others.

Not Just ‘What’ but ‘Who’

In the world of alternative proteins, there is much talk of ‘mainstream adoption’ and targeting ‘flexitarians’. Even as the sector faces headwinds based on consumer sentiment, inflation, and the economic downturn, industry champions cite the growth in plant-based foods, meager as it may be (America, the most advanced plant-based protein market, grew 6% and 7% in 2021 and 2022, respectively). With U.S. plant-based retail sales at $8 billion, this type of growth is hardly inspiring as alternative proteins try to disrupt a multi-trillion-dollar animal products market. At this growth rate, the industry will fall well short of the 30-60% predicted market share for alternative proteins by 2050.

To understand the arc of innovation toward mainstream adoption, we must look to products in the sector that have achieved addict status along with consumer segments that have made the leap. To be clear, we are not referring to consumers who purchase these products periodically, but those that have adopted them as their primary, even exclusive, choice. In the entire plant-based sector, one example shines above the rest: plant-based milk. The category commands an impressive 16% market share in the U.S., compared to a paltry 1.4% for meat substitutes. Since the alternative protein industry is focused on taste and price parity, it is especially curious that plant-based milk doesn’t even come close to tasting like cow’s milk and is more expensive.

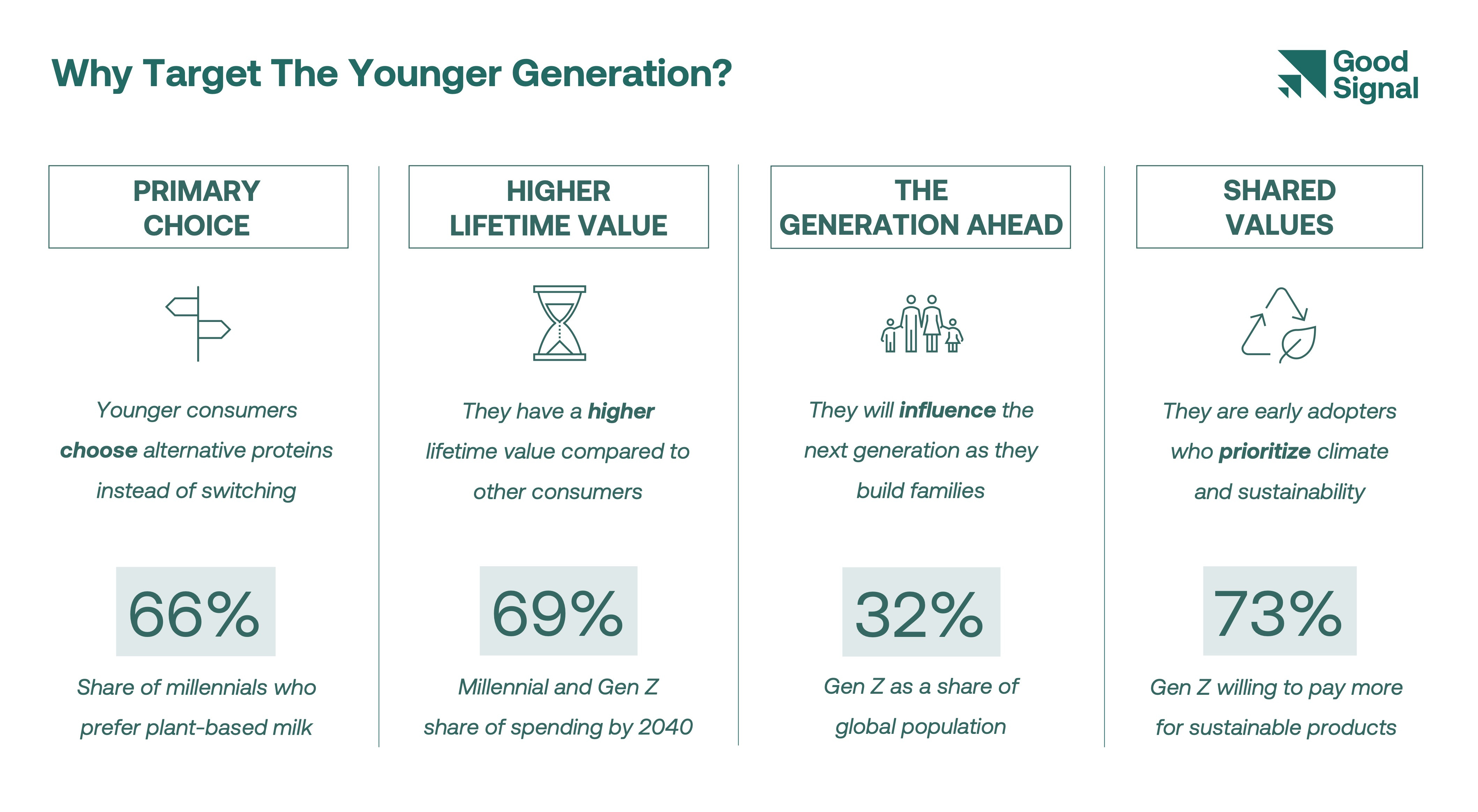

When we examine who has adopted plant-based milk, again, one segment stands out: younger consumers. As early as 2017, consumers in the United Kingdom between the ages of 16 and 24 (Generation Z) were consuming 550% more vegan milk than their older counterparts2. In the U.S., 66% of millennials cite that they prefer plant-based milk in stark contrast to just 19% of adults aged 55+3. Half of the millennials said they stock more than one kind of milk, including 22% who said they keep three or more types4. Gen Z bought 20% less cow’s milk than the national average last year5. Half of adults aged 55+ say they never consume non-dairy alternatives, as opposed to just under 8% of 18-34-year-olds who say the same. It is not surprising, then, that only 10% of older adults consume plant-based alternatives multiple times a week, compared to about one-third of younger people6. With dairy, the trend is so prevalent that younger consumers are termed the ‘Not Milk’ generation7. There is even talk of ‘milk shame’, where younger consumers view their peers consuming cow’s milk unfavorably.

This success has created a compounding effect for the category. Oat milk is projected to increase at a Compounded Annual Growth Rate (CAGR) of 14.2% through 20288. Blue Bottle made oat milk its default milk across its cafes in the U.S. one year after its pilot in mid-20219. Starbucks removed the surcharge on plant-based milk across its 150 outlets in Germany10. Large CPG companies like Nestlé, Chobani, and Danone are investing in the dairy alternative category with new products. The U.S. Food and Drug Administration (FDA) said plant-based milk can be labeled as ‘milk’ (as long as nutritional disclosures are provided on the packaging)11.

Alternative milk is accelerating the long-term trend of declining milk consumption. Americans’ annual milk consumption peaked at 45 gallons per person in 194512. By 2001, it was nearly halved to 23 gallons and reached approximately a third of its peak of 16 gallons by 2021. There are varying factors behind these trends. One key driver is lactose intolerance. Experts estimate that 68% of the world’s population is lactose intolerant (even if many don’t know it)13. In Asia, the numbers are even more stark — an estimated 90% of adults in East Asia and 80% in Central Asia have an impaired ability to digest lactose14. Another factor is the proliferation of beverage choices, leading to declining milk consumption during afternoons and evenings. Younger generations are also shedding milk due to sustainability concerns. Protecting the environment and climate change remains the top concern for Gen Z, with 73% of Gen Z consumers willing to pay more for sustainable products, more than every other generation15.

Targeting The Younger Generation

If the younger generation embracing plant-based milk is the singular example of addictive behavior in the alternative protein sector, we must ask ourselves: where’s the next opportunity? To reach mainstream adoption of alternative proteins by 2050, we must recognize that the younger demographic has already demonstrated that it is more open to alternative proteins compared to generations that preceded them. There are significant benefits to targeting them:

They choose, not switch: Unlike targeting older consumers, who have had longstanding patterns of consuming conventional animal products, the younger generation doesn’t have set benchmarks. Imagine targeting consumers who are yet to fully form their views on what to consume, and even what constitutes ‘meat’ or ‘milk’. As they make these choices independently for the first time, it puts alternative proteins on an even footing with animal products.

They have a longer runway: Since younger consumers have the highest number of years of purchasing power ahead and the largest customer lifetime value, winning a consumer earlier in their life has far greater benefits relative to someone who has fewer years of consumption ahead. Further, this is a growing market since their purchasing power rises as they age.

They will ‘pay it forward’: As these younger consumers build their own families, they are likely to expose them to alternative proteins, which will then create a new generation of consumers who will continue to prefer these products. Their heightened use of technology also enables broader visibility via social media and related tools.

They have shared values: Millennials and Gen Z consumers place a much higher priority on sustainability and animal welfare than older consumers. Climate change and the environment rank as the top concern for Gen Z, more than any other generation. Their higher alternative protein adoption rates demonstrate precisely this dynamic.

Yet, targeting the younger generation pays dividends but requires a unique approach. Surveys indicate that they care more about sustainability and price, whereas older consumers care more about health. They are also technology savvy, and far more interconnected as a result. Conventional dairy, following their iconic Got Milk? campaign a generation ago has renewed its efforts with new initiatives including Gonna Need Milk and Wood Milk. The alternative protein industry must be equally savvy and aggressive.

From Novelty to Loyalty to Addiction

Although it has garnered less than 2% market share of animal products, the alternative protein industry has come a long way in a short time. It has made significant progress in creating innovative products and engaging every part of the ecosystem, most notably consumers, to build a more sustainable and equitable food system. Given its limited resources, it is crucial for industry participants to direct their efforts to areas that provide the highest leverage and return on capital. In this respect, it is worth considering whether a consumer adopts these products as a novelty, a loyal customer, or an addict.

The younger generation has indicated its propensity to consume alternative protein products as early adopters, fueled by shared values and a fresh perspective about foods that constitute their diet. They are also growing in numbers. As of 2019, Gen Z became the largest segment of the global population, constituting 32% of the total16. There are also numerous benefits to targeting them given their rising purchasing power and long consumption runway. Yet, this requires a directed approach with specific strategies. Winning younger consumers will require a unique set of product formats, brand messaging, and channel development. Products will need to be priced more competitively, speak to topics that these consumers are about, and require tech-savvy marketers. The animal agriculture industry is far ahead in this regard. To win market share for alternative protein products, it is not possible to target all consumers. The advantages of targeting younger consumers are difficult to ignore. As the industry looks ahead to the next decade, and onward to 2050 with a view of achieving 30%+ market share with mainstream adoption, it is not just about getting 3 out of 10 people to consume these products; it’s about which 3.

MarTech Zone

Plant-Based News

Civic Science

Morning Consult

The New York Times (NYT)

International Food Information Council

NYT

Grand View Research

Blue Bottle Coffee Blog

World Coffee Portal

FDA, Draft Guidance on Labelling of Plant-Based Milk Alternatives and Voluntary Nutrient Statements

U.S. Department of Agriculture (USDA), Economic Research Service

U.S. National Institute of Diabetes and Digestive and Kidney Diseases

DSM Insights

CNBC

New York Post