The Flywheel: Scaling the Alternative Protein Ecosystem

“The chain is only as strong as its weakest link, for if that fails the chain fails and the object that it has been holding up falls to the ground.”

– Thomas Reid

The theory of constraints is a management principle that essentially states that achieving any goal is usually limited by a small number (or often a single) constraint. Put more simply, it says that “a chain is only as strong as its weakest link”, and that to make the chain stronger (that is, to achieve a goal), an individual or organization must focus on the weakest link. The plant-based food industry is early in its development. Like a teenager, it exhibits an exuberance of youth with its eagerness, excitement, and enthusiasm. Despite recent headwinds, the industry continues to believe its fortunes will not just endure but thrive. Though valuations have plummeted, and the money flow has ebbed, there somehow seems to be a belief that the show will go on.

Consumers are increasingly asking why they should pay more for products that don’t match up in taste and have questionable health benefits. This naturally leads to decision makers in retail and food service outlets to wonder how much space on the shelf and the menu these products deserve. Producers, including startups and large food manufacturers alike, are still contending with an anaemic supply chain that hasn’t yet delivered the raw materials to produce the next generation of products and are wrestling with scale-up challenges. Investors that are not mission-driven, who will ultimately bring most of the money if the industry is to scale, are no longer seeing compelling exit valuations. Governments are expected to step in with regulatory pathways and funding, but battles with both safety and labelling are ongoing. And the industry faces a severe talent shortage, especially with technical and more experienced workers.

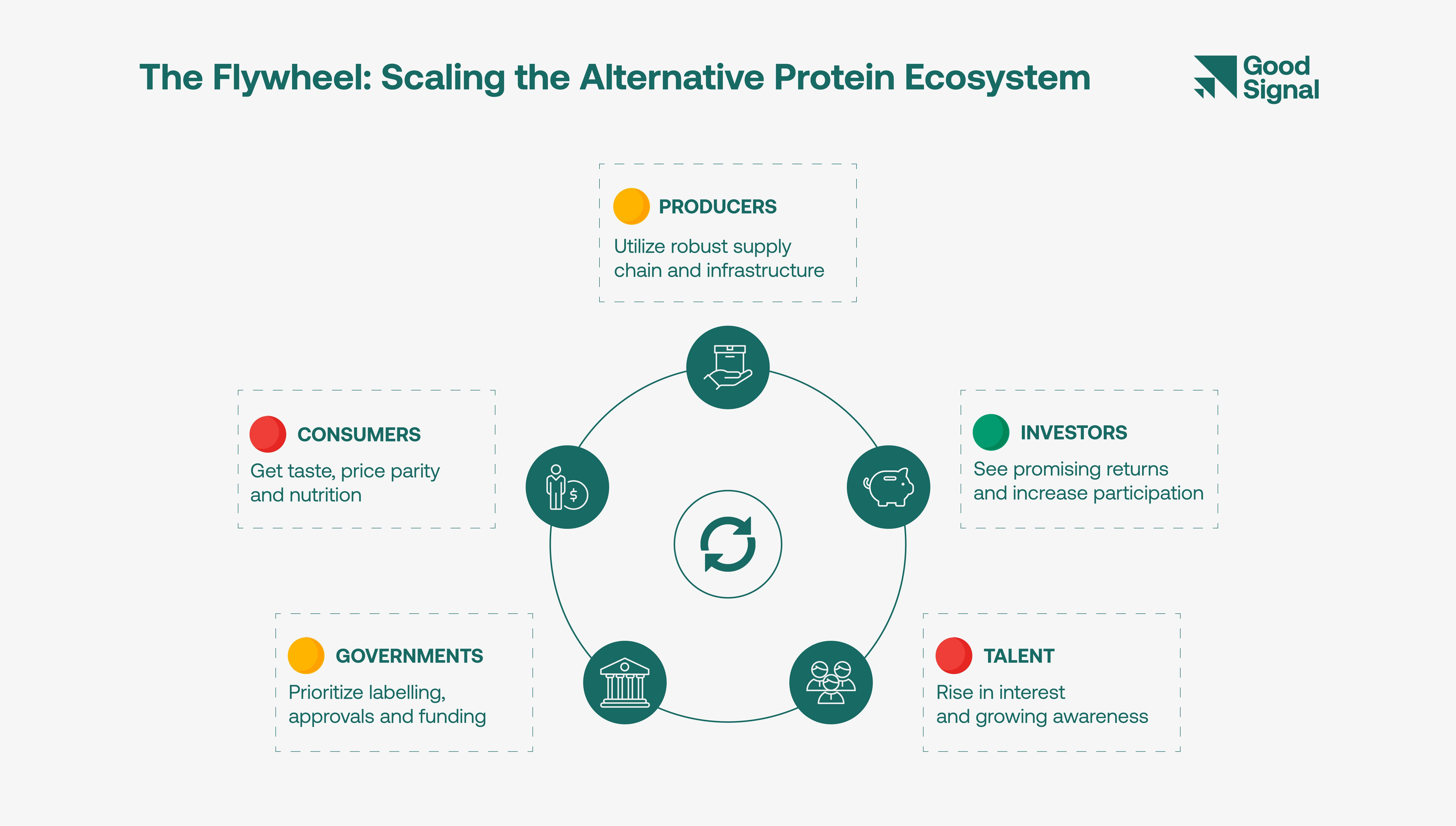

What gives us confidence that alternative proteins will be a growth market, after all? To be sure, there is much to be proud of. A watershed funding year infused $5 billion into the industry in 2021.1 While the plant-based meat sales were flat last year, the industry has been on an upward trajectory for the last few years. There is traction from both health-conscious consumers as well as startups focused on plugging gaps in the supply chain. The IPO window will reopen, and regulatory approval for cultivated meat is widely expected in the U.S., an event whose impact is difficult to overstate in its significance to the sector. But for the industry to succeed, it is crucial to understand the engagement and buy-in of key stakeholders – consumers, producers, investors, governments, and talent – and identify the weak link(s) in the chain. Only with deliberate focus can we make them stronger and enable the industry to reach its potential. As each of them gain strength, they reinforce one another to create a ‘flywheel effect’ that propels the industry forward. There are other stakeholders, such as non-profits, and universities, but in this article, we take a closer look at those mentioned so far, and chart their relative progress as green, yellow and red below.

Consumers — ‘have my cake and eat it too.’

Plant based sales have stalled. Let’s examine recent activity in the most advanced market for alternative proteins, the United States. In 2021, one-year dollar growth sales for plant-based meat were 0%.2 A Deloitte survey revealed that the number of consumers who buy plant-based meat for themselves or a household member did not grow in 2022. Today, the sector is driven by flexitarians, who in turn are driven by health. When asked about motivations for purchasing plant-based foods, 91% of Americans cite health as being at least moderately important to them.3

Historically, consumers have been driven by three key factors: taste, price, and health. Sustainability remains a distant fourth. Since market for alternative proteins provides substitutes for animal products which people find delicious, the bar for taste has already been set — consumers want products to taste like meat, seafood, dairy, or eggs. No one is complaining that beef or milk doesn’t taste good enough. It should not be surprising, then, that two-thirds (67%) of Americans say they would be willing to eat more plant-based foods if they tasted better. When it comes to price, more than half (58%) of Americans say plant-based meat is too expensive, while 63% say they would be willing to eat more plant-based foods instead of meat if they cost less than the real thing.4 And price elasticity of demand is high – just a 1% decrease in price results in a 3% increase in market share.5

Each successive band of improvement in taste, price and health will result in a greater segment of consumers adopting alternative proteins. But to do so, the industry must develop products that are better than what’s available today, at a cheaper price, with a better nutritional profile. For this, we will need not just incremental innovation, but fundamental leaps forward, aided by an improved supply chain, better manufacturing capabilities, and fermentation and cultivated technology stacks coming online. Winning the mainstream consumer’s wallet is far from certain and will require sustained effort.

Producers — ‘hope springs eternal’

Alternative protein producers, which include startups and large food manufacturers alike, seem to have hit a wall trying to achieve taste and price parity with animal products. We need new technologies to create a new generation of products to meet promises made to consumers. Today, the supply chain for the sector is anaemic at best. Plant-based food manufacturers have a limited set of raw materials along with equipment and infrastructure built for an entirely different set of products. Cultivated meat companies are having to devise their own substitutes to fetal bovine serum, the most expensive component of the production process.

To make matters worse, the path to scaling up is a tenuous one. For plant-based meat, the Good Food Institute (GFI) estimates that to meet the demand for just 6% of the meat sector would require construction and operation of facilities costing roughly $27 billion in global capital expenditure and at least $17 billion in annual operating costs.6 Cultivated meat companies are having to devise entirely new solutions, as the pharmaceutical sector created scale based on high prices and low volume. Sadly, the food industry has economics that are precisely the opposite: high volume and low prices. This will require not an incremental change, but a fundamental rethink of the infrastructure required. Cultivated meat companies have the further complication of an uncertain regulatory pathway. Both the EU and Singapore have developed their respective novel food regulations wherein the processing time for each application can take 9-12 months for each new product.

Fermentation fares no better. An estimated 95% of precision fermentation facilities are outdated or not suitable for food production. Further, more precision fermentation capacity was lost in 2021 than added. Much of the 61 million litres of fermentation capacity available for use globally is already under contract. Of the remainder, just 2 million litres have the downstream processing capability necessary for food applications, a fraction of what is required in the coming years.7 In addition, fermentation capacity in the hands of multinationals is typically reserved for more lucrative products such as pharmaceuticals.

As a result, plant-based companies are following the market (primarily the U.S.), fermentation companies are following capacity and cultivated companies are following the regulatory pathway. We need innovative startups to bridge the supply chain and infrastructure gaps to pave the way for the industry to move forward.

Investors — ‘show me the money’

There is much talk about mission-aligned investors who genuinely want to make an impact and improve the food system, but little talk about the ruthless nature of the investment business. Despite the best intentions, if capital deployed does not generate compelling return, it will not be redeployed. This harsh truth is reverberating across the sector as markets descend back to reality. The twin flagships of the industry in the public markets, Oatly (NASDAQ:OTLY) and Beyond Meat (NASDAQ:BYND), have plummeted from a market cap to sales ratio of 30x down to 2x today, with the latter eliminating 19% of its workforce this month.8

This has significant implications for stakeholders across the sector. Investors don’t see returns, and question making further investments. This is especially true for multi-sector investors, who will ultimately deploy most of the capital in the sector. Employees’ stock options are underwater, leading them to rethink their compensation. With depressed valuations, companies can no longer utilise their capital to make acquisitions or raise additional capital inexpensively. And startups won’t have a benchmark for attractive valuations they can use to raise capital or access public markets. The industry desperately needs an expanded base of public companies which provide coverage across technology stacks (e.g. fermentation, cultivated), different types of customers (e.g. business-to-business) and new product categories (e.g. seafood, eggs). The industry would benefit from a new flagship in the public markets that showcases the opportunity in the sector.

For the private markets, it’s crucial to engage a broader base of investors. Around the sector are three other industry groups that have deep interest in alternative proteins — agri-food, biotechnology, and sustainability / climate-technology. The alternative protein sector received roughly 10% of total investment in the agri-food sector in 2021. During the same period, the agri-food sector overall received $51.7 billion9, biotech received $34.8 billion10 and sustainability / climate-tech received $53.7 billion11. Ultimately, the sector must meaningfully tap the broader venture capital market with investors that are not just mission-driven to tap global venture funding, which was a jaw-dropping $330 billion12 in 2021.

Governments — ‘you have to see it to believe it’

In December 2020, the Singapore Food Agency (SFA) approved a ‘novel food petition’ for cultivated chicken produced by Good Meat (part of Eat Just) to be sold in Singapore as an ingredient in its nuggets. In doing so, it created the most advanced regulatory pathway in the world for the sector. Almost two years hence, no other government has matched it. Its further approval of a gas fermentation based protein from Solar Foods marks another key milestone. The Dutch government recently allowed tastings of cultivated meat under controlled conditions. A joint regulatory framework between the U.S. Department of Agriculture (USDA) and the Food and Drug Administration (FDA) is poised to open the door for the sector, but it’s hard to tell when this will occur. As a result, while the U.S. is leading the sector in innovation, Asia has taken the lead in terms of regulatory pathway.

This has not stopped governments from opening the spigot for funding. Singapore and Australia have allocated over $100 million across selected themes in agri-food where alternative proteins are featured prominently. South Korea has done something similar with a budget of $70 million. The Netherlands announced it will allocate €60 million to support its cellular agriculture ecosystem. Israel provided $18 million to the cultivated meat consortium in the country. In the U.S., the government plans to invest more than $2 billion in the U.S. biotechnology sector, which will significantly benefit alternative proteins. The USDA also awarded $10 million to Tufts University to form a new National Institute for Cellular Agriculture.

Labelling has been another battleground, fuelled by powerful lobbies in the animal agriculture industry. Countries currently considering or moving forward with labelling restrictions include the United States, Canada, Argentina, Brazil, Ecuador, France, Norway, Turkey, South Africa, Japan, India, Australia, and the EU. GFI, ProVeg and the Plant Based Foods Association deserve credit for defeating proposals for labelling bans for meat and dairy in recent years in both the U.S. and EU. Organisations in other countries are doing similar work which is essential for the sector.

Talent — ‘where’s the beef?’

The sector is fortunate to draw a talented workforce that has created the first phase of innovation in the sector, giving it worldwide visibility and hope for a better future. However, these companies are struggling to find workers, particularly those in technical and more experienced managerial roles. Over 30% of respondents in our recent startup survey ranked recruiting as the biggest challenge to their business, on par with fundraising. 62% mentioned that technical talent was difficult to find while 46% cited similar challenges with the director or manager level.13 The top 20 firms in the alternative protein industry have nearly 200 job openings.14

It will take time to grow talent indigenously in the sector. In the interim, we will need to fill the gap from other sectors such as the biotechnology and pharmaceutical industries. This is unlikely to provide relief. In the U.S., a bellwether for the sector, unemployment is nearing a fifty-year low, signalling a labor shortage. A recent survey of top pharmaceutical and biotechnology companies revealed that although graduates with degrees in biotechnology grew 56%, job openings doubled during this time. For advanced degrees, PhD graduates in biotechnology rose 16% while open positions surged 43%.15

We cannot grow the sector without talent. The first set of workers arrived because of the mission. The next set of workers will invariably come because of career opportunity. Labor market trends indicate this talent will have many options as they chart their careers. We must ensure alternative proteins represent a compelling choice.

Turning The Flywheel

In his seminal book, Good to Great, Jim Collins highlights that the path to success (for a company, or indeed a sector) doesn’t come as the result of a single intervention or initiative, but rather from the accumulation of little wins that stack up over years of hard, painstaking work. He states that the ‘flywheel effect’ occurs when the momentum of these accumulated wins takes over to power a sustained period of growth.

The flywheel is just starting in the alternative protein sector. Each stakeholder has a crucial role. Investors have started to pour in money, but we must utilise this capital to build products that consumers want. That will require heavy investment in both the supply chain and manufacturing capabilities. Governments must recognise that there is no sector with a wider set of implications which span food security, human health, animal welfare, resource usage and climate change.

The domains that have been the most challenging for the sector – consumer sentiment and talent acquisition – deserve particular attention. Red lights in these areas, or with any other, will stop the flywheel. Our focus must remain on the components that create maximum leverage, which will ultimately create the fastest growth trajectory for the industry. It’s exciting to see how far the industry has come; to move ahead, each stakeholder, with their unique interests and concerns, must thrive.

Good Food Institute

Good Food Institute

Yale Program on Climate Change Communication

Yale Program on Climate Change Communication

Meat Demand Monitor (MDM)

Good Food Institute

Warner Advisors

Public market data

AgFunder

McKinsey & Co.

BloombergNEF

Forbes

Good Signal survey

Public job postings

Boston Globe