Jumping the Curve: A Journey of Deep Tech Innovations

"Success is not final, failure is not fatal: It is the courage to continue that counts."

– Winston Churchill

The advent of new technology is laced with challenges. Pioneers face obstacles spanning technology, regulation, and market acceptance. Both established industries and consumers resist change. Successful innovators must not only create superior products, but also educate the market, build trust, and navigate regulatory frameworks. Although new technologies have the potential to transform sectors and drive societal progress, their adoption curve is anything but smooth.

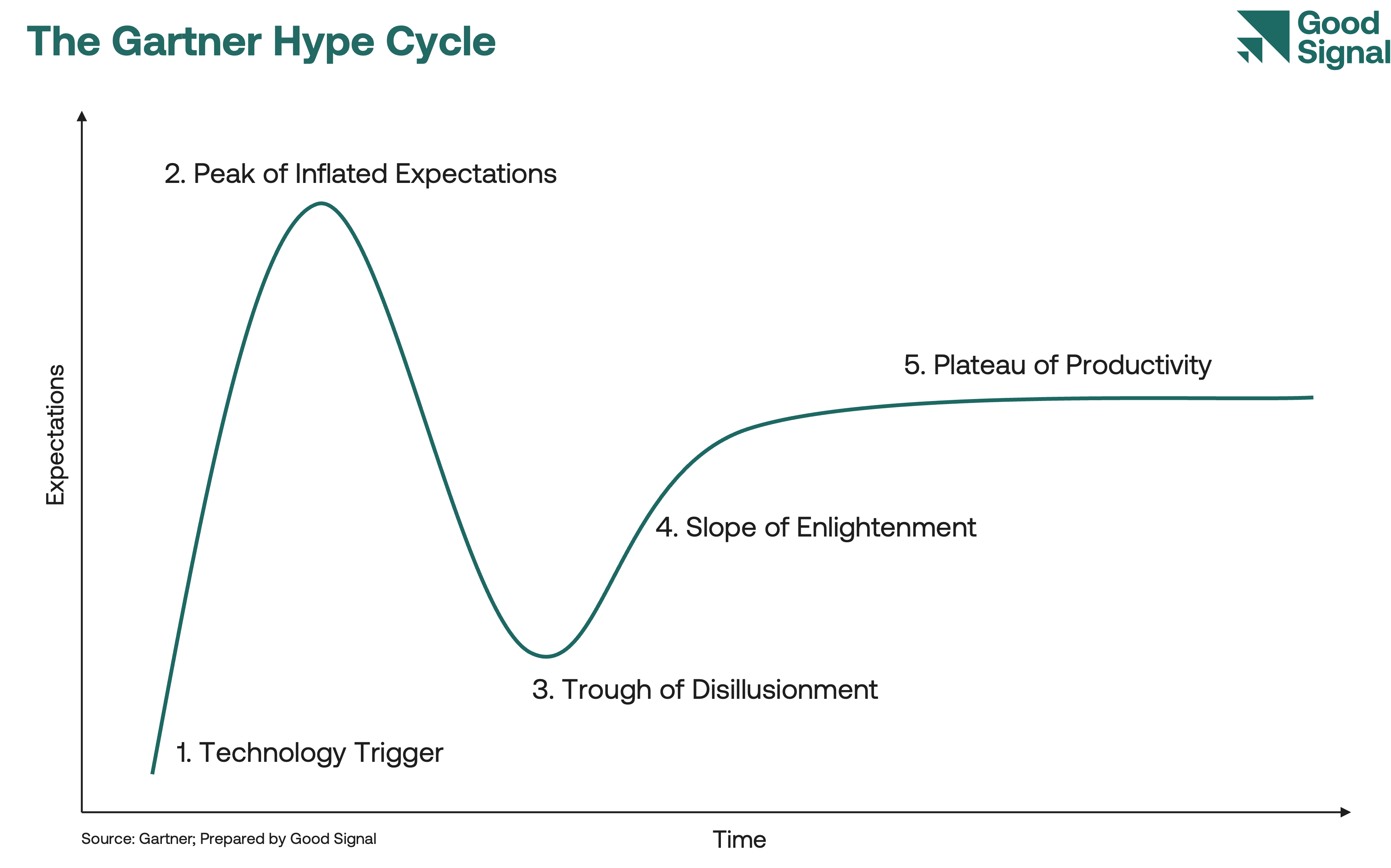

The Gartner Hype Cycle is a potent framework for examining any technology evolution. It maps an emerging technology into several phases:

Innovation Trigger: An innovation sparks consumer interest.

Peak of Inflated Expectations: Hype created by media and other stakeholders overshadows reality, resulting in unrealistic expectations.

Trough of Disillusionment: Skepticism emerges as the technology fails to deliver on unrealistic expectations. This is often accompanied by media predicting the technology’s demise.

Slope of Enlightenment: Consumers reset their expectations even as a better understanding of the technology leads to incremental improvements that bridge the gap between hype and reality.

Plateau of Productivity: A new generation of products emerge that address consumer needs. Consumers find utility as products undergo gradual improvements in response to feedback.

Meatless Mania

As a relatively nascent industry, the alternative protein sector has not been immune to this hype cycle. With the founding of Beyond Meat in 2009, the first plant-based burger was the trigger that sent expectations soaring. Precision fermentation and cultivated meat technologies promised to produce meat replicas with a fraction of the resources, without animal slaughter, and with significantly lower emissions. Impossible Foods introduced burgers that could “bleed” like real meat. However, early versions of these products fell short of consumer expectations when it came to price, taste, texture, and nutrition. This sent the industry tumbling down, leading the media to raise questions about both the industry and its products. As the alternative protein industry navigates these challenges, it is worth exploring whether the industry will transition out of the trough of disillusionment. Instead of attempting to predict an uncertain future, we look to other industries that have navigated the hype cycle and examine the tailwinds supporting each sector to uncover valuable lessons.

Image Credit: UladzimirZuyeu/Shutterstock

High Voltage – The Story of Solar Technology

The story of solar photovoltaic (PV) technology mirrors the classic path of many transformative innovations, navigating through the stages of the Gartner Hype Cycle.

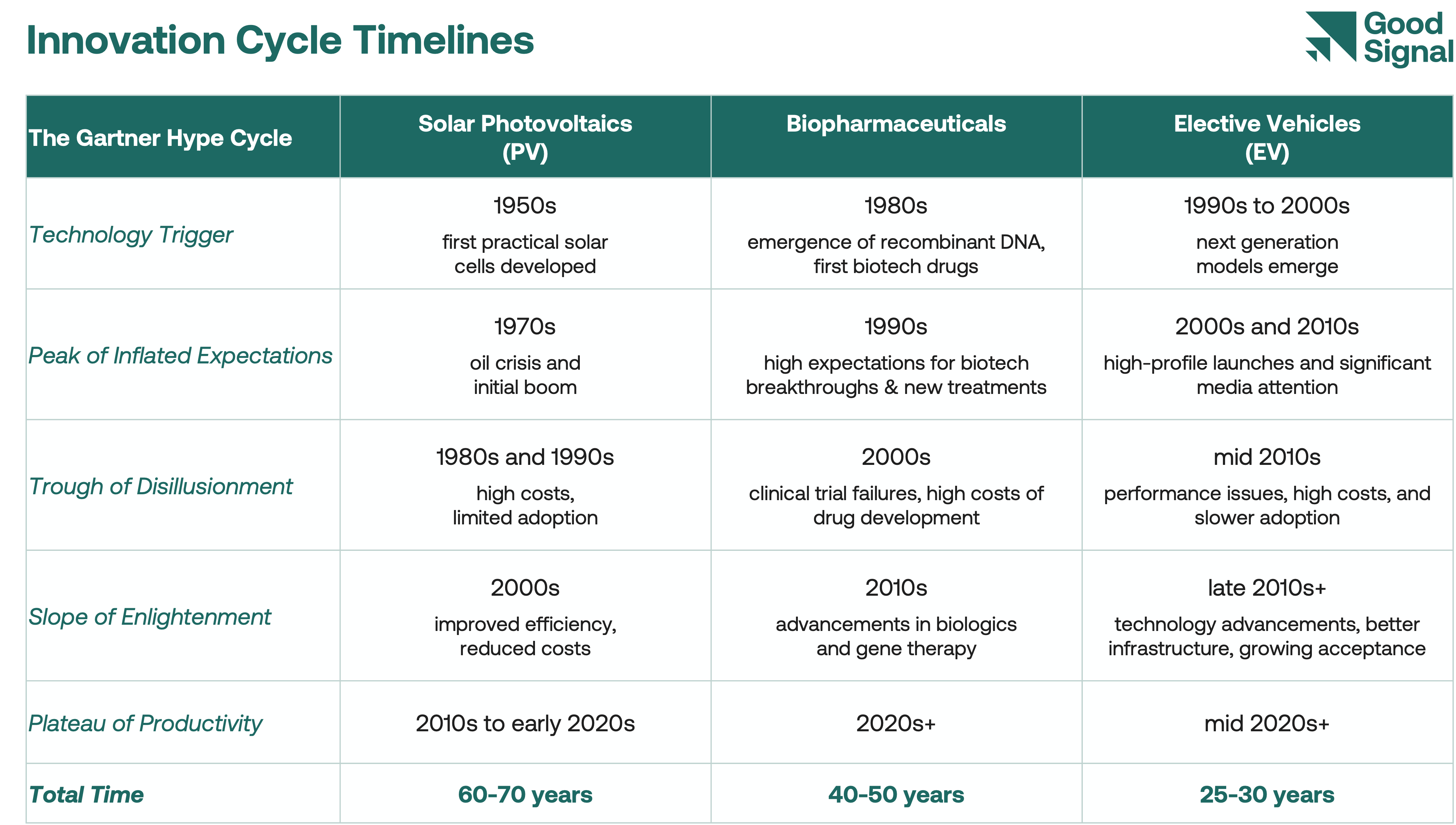

The Technology Trigger for solar PV began in the 1950s when the first practical solar cells were developed. These early cells were a breakthrough in harnessing the sun’s energy, and this pioneering work set the stage for future advancements.

The 1970s saw a surge of excitement for solar PV, fuelled by the global oil crisis leading to the Peak of Inflated Expectations. With soaring energy prices, solar PV was heralded as the answer in the quest for alternative energy sources. Governments and companies launched ambitious initiatives, and the media painted a picture of a solar-powered future. While expectations soared, solar technology was still in its infancy, lacking the efficiency and the infrastructure needed to support its widespread adoption.

Early excitement for solar PV began to fade in the 1980s and 1990s. The high costs of solar panels, combined with slow adoption rates and the challenge of integrating solar energy into the grid, led to frustration. Many viewed solar as an impractical energy source, and several companies in the space struggled to survive. These headwinds led the industry to a low point by the end of this period.

In the 2000s, solar PV began to evolve. Technological advancements led to increased efficiency, and manufacturing processes became more cost-effective. The price of solar panels dropped, making them more accessible. Government incentives for renewable energy helped further spur adoption. As economies of scale were realized, applications for solar power grew, and the once-promised vision of solar becoming a mainstream energy source started to take shape.

Solar PV reached the Plateau of Productivity in the 2010s to early 2020s, becoming a mature and widely adopted technology. The costs of solar power have dramatically decreased with greatly improved efficiency of panels. Solar power is now a meaningful contributor to global electricity generation, contributing 5.5% of global electricity in 2023.1 According to the International Energy Agency (IEA), Solar PV accounted for three-quarters of renewable capacity additions worldwide in 2023. Major strides in energy storage technology, such as improved battery solutions, have accelerated solar adoption, with governments around the world setting ambitious goals to further expand renewable energy. The total time from the initial innovation trigger to this plateau has been approximately 60 to 70 years.

Injecting Growth – The Story of the Biopharmaceutical Industry

The journey of the biopharmaceutical industry is one of high expectations, significant setbacks, and remarkable breakthroughs.

The Technology Trigger for biopharma came in the 1980s, with the emergence of recombinant DNA technology and the creation of the first biotech drugs. The first recombinantly produced human insulin was introduced under the brand name Humulin in 1982,2 and excitement around the innovation sparked hope for a future where biotechnology could revolutionize healthcare.

With the rapid development of genetic research and high-profile drug discoveries, the industry was brimming with optimism at the turn of the century. Bold predictions were made about the potential for biotech to cure genetic disorders, create personalized medicines, and transform the treatment landscape. Inflated expectations led to heightened investment in biotech. Numerous companies went public, promising world-changing breakthroughs.

Unfortunately, innovation progressed slower than anticipated as developing effective, safe treatments involved unforeseen challenges. The industry grappled with high drug development costs, regulatory hurdles, and failures of clinical trials, leading to a low point in the early 21st century. Several biotech companies struggled to bring their products to market. It became clear that the path from discovery to market was longer, more expensive, and more uncertain than initially envisioned.

The biopharma industry began to recover in the 2010s, driven by advancements in biologics, gene therapy, and targeted treatments. The success of drugs like monoclonal antibodies and the rise of CAR-T cell therapies3 brought new hope. The introduction of gene-editing technologies like CRISPR4 opened new possibilities for treating genetic disorders at their root cause. These success stories generated a flywheel effect. While challenges remained, the industry began to find its footing with more targeted therapies showing promising results, signaling the emergence of the Slope of Enlightenment.

The biopharmaceutical industry entered the Plateau of Productivity in the 2020s as advances in biologics, gene therapy, and immunotherapy moved from experimental to mainstream, with new treatments reaching patients faster than ever before. The industry’s swift response to COVID-19 by developing and deploying multiple vaccines within a year of the initial pandemic designation validated the potential of biotechnology and opened the door for new vaccine platforms and therapies. As the industry matures, the focus is shifting toward refining and scaling these innovations to improve patient outcomes on a global scale. The biopharma industry, once filled with uncertainty, now serves as a beacon of hope in modern medicine. The total time from the initial innovation trigger to this plateau has been approximately 40 to 50 years.

EVolution – The Story of Electric Vehicles

The launch of Electric Vehicles (EVs) marked the dawn of a new era in transportation, signaling a shift away from fossil fuel dependence toward a more sustainable future. While the first practical EV was built by William Morrison around 1890,5 modern EVs emerged nearly a century later with pioneering developments and the launch of early models like the GM EV1 and the Toyota Prius.

Expectations soared in the late 2000s with the introduction of Tesla’s Roadster and Model S, which generated tremendous excitement and lofty expectations about the potential of EVs to revolutionize transportation. However, this period also saw overly optimistic projections about the speed of mass adoption and the readiness of supporting infrastructure.

Following this peak, the industry experienced a lull during the mid-2010s. Challenges such as high costs, limited range, long charging times, and a lack of widespread charging infrastructure tempered early enthusiasm. Many early EV startups faced financial difficulties, and consumer adoption lagged behind expectations.

Persistent innovation and gradual improvements marked the industry’s climb up in recent years with advancements in battery technology, economies of scale, and increasing governmental support via incentives and emission regulations. Automakers expanded their EV offerings, and charging infrastructure grew substantially.

The industry is entering the Plateau of Productivity with EVs accounting for roughly 10% of total new car sales in the United States in 2023.6 Other markets are seeing even more rapid EV adoption. The total time from the initial innovation trigger to this plateau has been approximately 25 to 30 years. However, the road has been a bumpy one.

Cautionary Tales

While many technologies have successfully navigated Gartner’s Hype Cycle, albeit over varying timelines, there are industries and innovations that remain mired in the Trough of Disillusionment for extended periods, struggling to overcome practical, economic, or adoption challenges. Two such examples come from the green fuel industry – biofuel and hydrogen fuel electric vehicles.

Biofuel: Modern biodiesel fuel is an outcome of research conducted in the 1930s in Belgium. During the early 2000s, biofuels, particularly ethanol and biodiesel, experienced the Peak of Inflated Expectations driven by global energy security concerns and climate change mitigation efforts. However, the late 2000s and early 2010s saw many biofuel startups fail or pivot their business models7 as the industry struggled to maintain momentum due to several factors:

Economic Viability: High production costs and competition from cheaper fossil fuels have limited widespread adoption.

Environmental Concerns: Some biofuel production methods, such as those involving large-scale cultivation of crops like corn and palm oil, have been criticized for their impact on emissions, food security, deforestation, biodiversity, as well as land and water usage.

Technological Challenges: Second- and third-generation biofuels, which rely on non-food crops or waste, have faced difficulties scaling up and reducing production costs.

Although advanced biofuels (e.g., those derived from algae or cellulose) along with waste-to-energy approaches for biofuel production offer promise, progress has been slower than expected. Some technologies remain in pilot phases or are used on a limited scale, suggesting the industry has not yet moved out of the Trough of Disillusionment.

Despite these setbacks, biofuels still hold potential, especially as governments and industries aim for net-zero goals. However, breakthroughs in cost reduction and efficiency will be required for the industry to regain its footing.

Fuel Cell Electric Vehicle (FCEV): As the most abundant element on the planet, Hydrogen has immense potential as an environmentally friendly and sustainable fuel source. The General Motors Electrovan, developed in 1966, was the world’s first hydrogen fuel cell electric vehicle. It sparked expectations for FCEVs by showcasing a ground-breaking technology that promised clean energy with water as its only emission. Its debut captured the public imagination and fuelled visions of a hydrogen-powered future despite severe practical limitations like high costs, bulky infrastructure, and safety concerns. While FCEVs like the Toyota Mirai, Hyundai Nexo, and Honda Clarity have emerged in recent years, slow adoption and technical hurdles have spurred skepticism about their viability for widespread consumer adoption. In 2023, only 14,451 FCEVs were sold worldwide8 and there are only about 17,000 hydrogen-powered vehicles on U.S. roads today. The key challenges for FCEV adoption include:

High Production Costs: Intricate technology and specialized equipment required lead to high production costs.

Low Energy Efficiency: Hydrogen leakage during transit and energy needed to liquefy hydrogen diminish overall energy efficiency.

Environmental Concerns: Industrial-scale production of hydrogen fuel often relies on fossil fuels, negating some of the environmental benefits associated with the technology.

Infrastructure Challenges: Lack of hydrogen refueling infrastructure limits widespread adoption.

Despite these obstacles, there have been significant advancements in hydrogen fuel cell efficiency and durability in recent years, driven by efforts from both private entities and public institutions. It remains to be seen whether FCEVs will achieve widespread adoption.

Lessons Learned

While each industry follows its own unique trajectory, these stories reveal several common threads:

Low Prices Trigger Demand: Cost reductions are crucial to the growth of any industry, often leading to a tipping point for broader adoption. The continual drop in solar panel prices has been central to the solar industry’s remarkable growth. Over the past decade, the price of solar electricity has declined by 89%. The key inflection point occurred when the price of solar modules fell below $1 per watt in the 2010s. At this price, solar power became economically viable for a much broader range of consumers.

Government Participation is Essential: The role of government funding, policy, and regulation is crucial in shaping the trajectory of industries. The EV industry, in particular, has greatly benefited from government funding, incentives, rebates, tax credits, interest subsidies, and support for charging infrastructure, among other forms of assistance.

Innovation Drives Progress: Innovators are constantly pushing boundaries despite challenges and setbacks. While both the biofuel and FCEV industries have yet to reach their plateau of productivity, innovators continue to make progress, whether through advanced biofuels or green and blue hydrogen. Successful industries are the result of countless small, successful iterations.

Success Begets Success: Success stories serve as catalysts, igniting momentum and fuelling growth. The biopharmaceutical sector witnessed multiple success stories in the 2010s, including the use of CRISPR-Cas9 as a gene-editing tool to treat sickle cell disease and the application of chimeric antigen receptor (CAR) T cell therapy to target cancerous mutations.

Cycles Getting Shorter: The pace of innovation and market dynamics is accelerating, with product cycles shrinking faster than ever. The PV industry took 60-70 years to reach the plateau of productivity, while biopharmaceuticals took 40-50 years. The EV industry reached this stage in just 25-30 years. The onset of AI and its applications across all industries will only heighten this pace.

Meatless Harvest?

Let’s re-examine the alternative protein industry through the lens of the learnings above. From the day the first lab-grown burger was produced for $330,000 in 2013, the industry has experienced more technological advancements and cost reductions than many other disruptive technologies. However, as of 2023, the average price premium for plant-based meat and seafood still remains 77% higher than conventional products, according to GFI. The price gap for precision-fermented ingredients and cultivated meat is even higher, but it is closing due to ongoing technological advancements, process improvements, and economies of scale. The inflection point will likely occur when these products either reach price parity or demonstrate superior taste and texture, establishing their value as premium, cleaner-label options. We continue to see ongoing innovation in both areas.

The progress of the alternative protein industry has occurred with limited support from the public sector to date. In contrast, public sector assistance has fuelled the growth of other novel technologies, including semiconductors, EVs, and biotechnology. According to the IEA, governments worldwide provided roughly $40 billion in direct purchase subsidies for EVs in 2022. That dwarfed the $635 million in total government support for the alternative protein industry in the same year. However, we are seeing the winds of change. During the COP28 gathering in 2023, the Bezos Earth Fund announced a $1 billion commitment to transform food and agricultural systems. The organization has since invested $100 million in three alternative protein centers across the globe. The alternative protein industry is also gaining regulatory support with cultivated meat now approved for sale in three countries – Singapore, the U.S., and Israel – with Hong Kong recently joining the ranks by allowing sales. However, for the industry to achieve its full potential, governments must step up their support manifold.

Despite sector headwinds, innovation continues unabated. Founders are learning from the first generation of companies and evolving their approaches to meet current market needs. Entrepreneurs in the sector today are building companies that are specialists within the sector rather than the vertically integrated companies that preceded them. Instead of building expensive facilities, they prefer ‘capex light’ models, and are focused on near-term commercialization with the help of partners or contract manufacturers.

The alternative protein industry is increasingly embracing artificial intelligence (AI) to drive innovation and efficiency. AI is being leveraged for upstream strain engineering, optimizing production processes, developing new ingredients, and improving product formulations. AI is also being used to improve supply chains, reduce costs, and scale production. As it continues to evolve, AI will be a key enabler to drive progress in the alternative protein industry.

It is easy to dismiss the alternative protein sector because consumers didn’t like the first wave of plant-based products. However, it is worth noting that innovators are working relentlessly to fill the gaps. Much of the innovation hasn’t yet reached the hands (or mouths!) of consumers. Government support will further accelerate the industry. As the new generation of consumers begins embracing a new generation of products, it will signal the ascent of the industry on the Slope of Enlightenment and its eventual arrival at the Plateau of Productivity. With each passing day, we come closer to a time when ‘alternative proteins’ will simply be called ‘proteins’ as they see mainstream adoption.

As this will be our last article of 2024, we look to the future with cautious optimism:

From peak to trough, the hype cycle flows,

Traversing from euphoria to disillusionment’s lows.

Dust off and rise – EV, biopharma, and photovoltaics shine,

While biofuel and FCEV struggle, following a steep decline.

The environment for alternatives remains rough,

Rise like a phoenix or fade into oblivion – a situation tough.

The promise of comeback, tailwinds show,

But as the future unfolds, the world will know.

We thank you for reading Good Signal and wish you happy holidays! It has been our pleasure to be connected with you in our journey to distill insights from the sector.

Ember Energy

Alyas et. al. (2021), Human Insulin: History, Recent Advances, and Expression Systems for Mass Production

Mitra et. al. (2023), From bench to bedside: the history and progress of CAR T cell therapy

Broad Institute, CRISPR Timeline

U.S. Department of Energy, History of the Electric Vehicle

International Energy Agency (IEA)

Fortune Magazine

SNe Research Insights