A SWOT Analysis of Alternative Proteins

“Great results can be achieved with small forces.”

– Sun Tzu

The approval of cultivated meat for sale in the United States, achieved in the past month, is arguably the single most significant milestone in the history of the alternative protein industry. The reason, quite simply, is that cultivated meat represents the greatest challenge for the sector from the standpoint of technology, price, and regulatory approval. It also heralds its greatest promise – to use the power of technology to create bioidentical animal products from a lab! It signals what is possible, even probable, in the coming months and years, piquing consumer interest, and putting incumbents on alert. In retrospect, what seemed inevitable (or impossible) for those that had the luxury of observing from a distance, was in fact made possible by the hard work of a few with a grand vision, high capability, and unwavering persistence, who crossed hurdle after hurdle to reach this point. As we look ahead, first and foremost, we must recognize them for their tireless efforts to reach this historic milestone. It was anything but guaranteed and took years of effort along with hundreds of millions of dollars in funding. While cultivated meat has seen the limelight recently, its path was cleared by technologies that are further along in commercialization. Plant-based products walked, so fermentation technology could run, and cultivated products could fly.

So, what lies ahead? There is no doubt this is an inflection point for the industry. We are starting a new chapter where a new technology for creating ‘animal’ products is coming online. It is an excellent time to take stock as we enter the next phase of the sector’s development to both recognize its successes and understand what industry participants can do better. A SWOT analysis is a management tool to look at a sector, company, or even an individual from all angles by analyzing its Strengths, Weaknesses, Opportunities, and Threats. It was developed 50 over years ago but is no less potent in generating understanding and perspective today. Let’s look at a SWOT analysis of the alternative protein industry following the biggest milestone in its history.

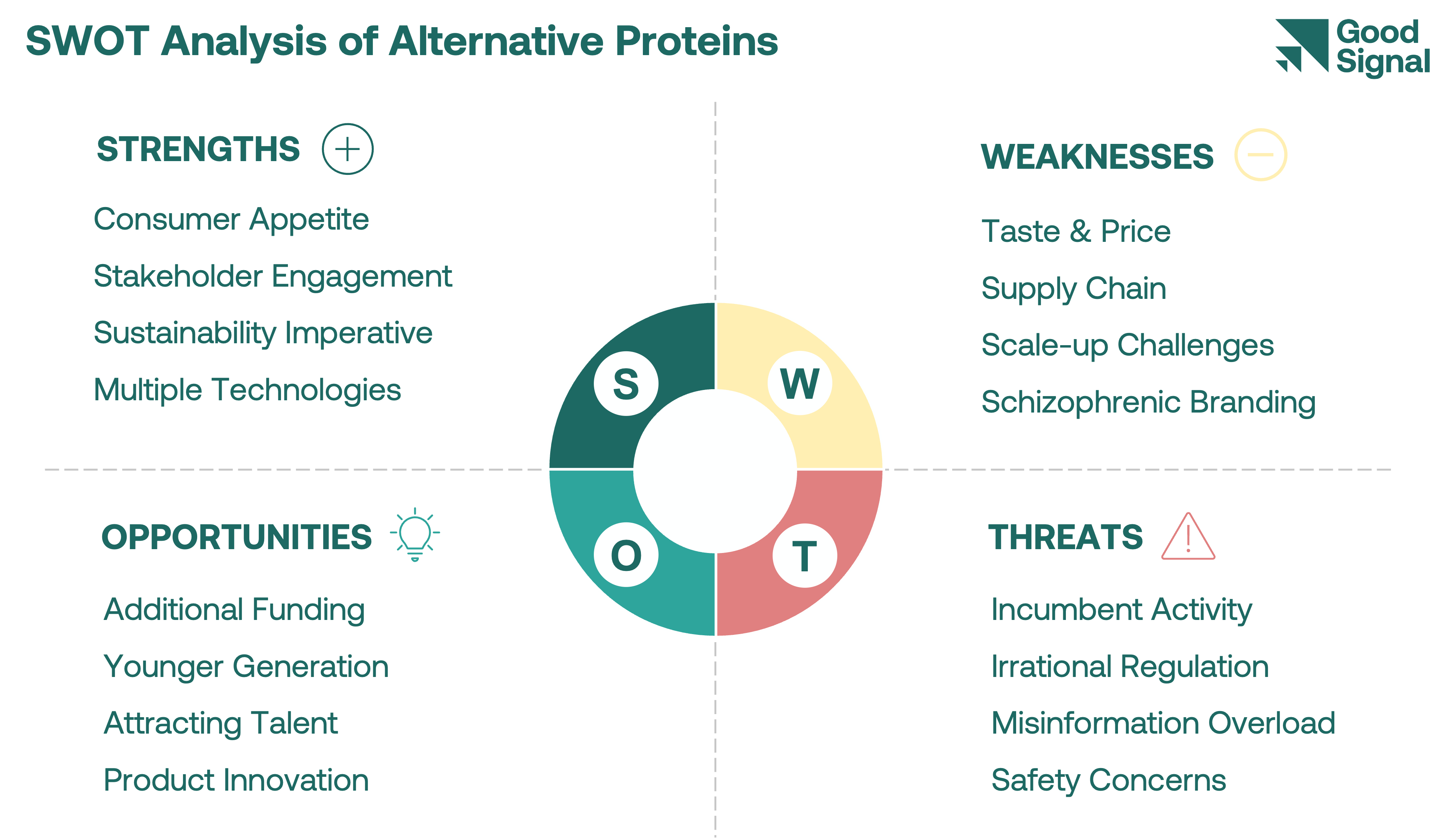

Strengths

Consumer Appetite

Even as the media complains about consumer sentiment, plant-based foods are acknowledged to be a long-term trend. A global flexitarian movement is thriving with 42% of the world’s population seeking to eat more plant-based food1. Alternative milk has seen the greatest success with a double-digit percentage of market share both in the U.S. (16%)2 and globally (12% for alternative dairy)3. Other dairy categories such as plant-based creamers and cheese as well as plant-based eggs saw the highest YoY increase in market share in 2022. Plant-based meat has largely convinced early adopters so far, but with new categories, products, technologies, and formulations on the horizon, it is only a matter of time before they meet consumer expectations.

Stakeholder Engagement

Whether it is governments, research institutions, non-profits, investors, incumbents, or start-ups, there is strong activity across all stakeholders in the alternative protein ecosystem. The economy and the funding environment may have slowed, but innovation hasn’t. According to Good Food Institute (GFI), governments across different geographies, have given over $1 billion in grants for research initiatives in the sector. Most leading consumer packaged goods and meat companies are involved in some capacity either through investments, acquisitions, partnerships, or developing and manufacturing products. The increased ecosystem engagement is fuelling innovation and growth in the sector.

A Sustainability Imperative

With a rising population and greater affluence, the demand for animal products is skyrocketing and sees no sign of abating, particularly in developing countries. Even if certain categories are seeing slowing demand, others are more than making up for it. Alarmingly, if we stay on the current path of animal product consumption, we face a protein shortage by mid-century4. Our food system is unsustainable. Alternative proteins represent the most promising path forward to bridge the protein gap by 2050. Therefore, alternative proteins are not optional; they are essential. Plant-based foods provide a 4.4 gigaton (Gt) reduction in CO₂ equivalent (CO₂e) emissions per trillion dollars of investment as compared to 0.4 Gt for vehicles, 0.3 Gt for electricity, and 0.2 Gt for aviation5. The animal products industry utilizes between 9 to 27 calories to deliver just one calorie for consumption6. A recent study from the University of Oxford found that vegans are responsible for 75% less greenhouse emissions than meat eaters, as well as 75% less land use, 54% less water use, and 66% less biodiversity loss7. The sustainability conversation will ensure that alternative proteins receive both attention and funding.

Multiple Technology Stacks

The sector is tapping the potential of not one, but three technologies, each of which brings a unique advantage. Plant-based technologies provide nutrition, fermentation enables the engineering of precision proteins, while cultivated creates bioidentical products with the same taste and texture that consumers demand. Further, new technologies such as molecular farming and plant-cell culturing are filling in gaps and creating new opportunities. To date, plant-based technologies have not been able to bridge the gap in taste and price. With the fermentation and cultivated technology stacks coming online, consumers will soon see higher-quality products.

Weaknesses

Taste & Price

Taste is king; price is queen. In the food industry, there is no getting around it. Even when the food system is transformed in the next three decades, this will ring as true then as it does today. To put it bluntly, the vast majority of alternative protein products available on the market today miss the mark on taste and cost more. Early adopters are forced to select the best of a series of mediocre choices that have limited appeal to mainstream consumers. The industry must learn that even if products aren’t identical to their animal-based counterparts, they must first and foremost taste great (think Oatly). And, they must be available at a reasonable price.

Supply Chain Challenges

The alternative protein sector runs on soy, wheat, and pea protein, with limited prospects for new protein options that can scale with increasing consumer demand. While options like chickpeas, fava beans, and mung beans are slowly making inroads into the industry, they invariably fall short on either protein content, production cost and yield, or palatability. Further, while the production quantity of the big three proteins has increased over the years, the price has gotten increasingly volatile. The average global price of soybean and wheat has been fluctuating erratically over the past decade with extreme highs and lows occurring more frequently. The price of soybean per metric tonne has ranged from $217 in 2006 to $570 in 2022, seeing an 11% decline to $508 in 2023. The over-dependency on these three ingredients limits product options and growth. To date, most of the funding in the sector has been received by companies focusing on end-consumer products. They may be sexier, but it’s hard to create great products without great ingredients. If the sector is to thrive, then its supply chain must thrive first.

Scale-Up Challenges

For the sector to scale, it will require not just additional innovation, but an immense amount of capital to fund its production requirements. A study by GFI concluded that the plant-based meat industry alone will require $27 billion in cumulative capital spending by 2030 to garner just a 6% share of animal products. This would need to be supplemented with $17 billion in annual operating costs. This is to say nothing of requirements for fermentation and cultivated products, likely to be even higher. The technological barriers to creating a replicable process will require exponentially more funding, access to capacity, and technological innovation as companies in the sector scale. Further, products are manufactured on legacy equipment using processes intended for other purposes developed decades ago. Innovation must be focused on these areas, to either improve efficiency of production or significantly increase the capital deployed towards infrastructure in order for the sector to scale up successfully.

Schizophrenic Branding

Despite consumer preference for taste and price, alternative protein start-ups have chosen to create brands around sustainability or scientific prowess. The tussle between messaging, highlighting sustainability, and cruelty-free production versus taste and price muddies branding and messaging for companies in the sector. Startups must be clear about the key message they want to convey to consumers. Is the key message that the product is sustainable or delicious? Is it better to highlight that the product is cruelty-free or economical? Food permeates our culture. Products must appeal not just to the logical and ethical aspects of consumer decision-making, but the emotional side as well.

Opportunities

Accessing Additional Funding

Through the economic boom, headlines persisted that the sector reached ever greater heights in funding. Unfortunately, there was little talk that this was a drop in the bucket. At its peak in 2021, alternative proteins took in $5 billion in funding for the year. Around the industry, there are three adjacent sectors – climate, biotechnology, and agrifood – each of which received over $50 billion in funding the same year. Climate-related funding, which has skyrocketed in recent years, offers a particularly compelling opportunity. Global warming is increasingly seen as the biggest near-term threat facing humanity, with animal agriculture responsible for 14.5% of total greenhouse gas emissions. Yet, alternative proteins receive relatively limited funding and attention compared to other sectors. There remains a significant opportunity to divert climate-related funding to the sector.

Targeting The Younger Generation

Ultimately, the sector must garner loyal customers, or better yet, addicts, who purchase products at a high velocity. Only plant-based milk has exhibited this characteristic within alternative proteins, specifically with younger consumers. There are a lot of benefits to targeting the younger generation, including their fresh perspective on food, a longer lifetime value, and a greater focus on sustainability. As early as 2017, consumers in the United Kingdom between the ages of 16 and 24 (Generation Z) were consuming 550% more vegan milk than their older counterparts8. Gen Z became the largest segment of the global population starting in 2019. This segment also cites climate change as its top concern, with 73% of Gen Z consumers willing to pay more for sustainable products9. If the sector only wins one consumer segment, then it must be the younger consumer.

Attracting Top Talent

As a bridge between agrifood, biotechnology, and climate, the sector offers talented workers a unique opportunity to both do interesting work and make a significant impact. In this sector, workers typically come because of an interest in food, science, or animal welfare. There are other reasons as well, such as addressing challenges we face with global warming, the environment, and our oceans. There is an opportunity to appeal to impact-driven workers in adjacent industries to address the talent gap in alternative proteins. This becomes especially critical when we consider that to scale, the industry needs workers with a broad range of expertise including research and development across different technologies, production scale-up, food safety, regulation as well as penetrating the complex distribution systems of the food industry globally.

New Product Innovation

Product innovation continues to thrive in the alternative protein sector, but there is room to do more. Much more. Today’s products largely try to mimic their animal-based versions, but is this the only path? Plant-based milks such as Oatly don’t mimic, but instead provide alternatives that taste similar (though not the same) and are delicious. If this is possible with milk, then why not other product categories? Perhaps there is an opportunity to create new products that are delicious alternatives to various meats. Taking things a step further, a ‘hybrid’ approach may fuse multiple categories (e.g. two types of meat) or integrate multiple technology stacks (e.g. plant-based and cultivated). New products must also increasingly address local tastes and preferences, which will appeal to a broader base of consumers, rather than being marketed globally. The industry must also be more aggressive with computational approaches using artificial intelligence and machine learning, which can significantly accelerate innovation and create solutions never before possible.

Threats

Organized Incumbent Activity

Incumbents in the industry are highly organized when it comes to influencing consumers, research institutions, or the government. Advertising programs in recent decades such as Got Milk?, Where’s the Beef?, Pork: The Other White Meat, and The Incredible, Edible Egg have been highly effective in shaping consumer behavior. These have been enabled by so-called industry check-off programs which promote the product category as a whole without any reference to individual brands. Similarly, incumbent lobbies have been instrumental in passing ‘ag-gag’ laws in several U.S. states, preventing the investigation of incumbent practices10. When dairy cooperatives in India and the U.S. run advertisements claiming that dairy farming is good for cattle and question the nutrients in plant-based milks, the industry must recognize that incumbents are likely to go to any lengths to retain market share, stoking consumer fears with misinformation if necessary. In contrast, it is curious that despite a link between processed meats and cancer, they continue to be sold in large numbers.

Irrational Regulation

Whether it is animal product subsidies to lower conventional meat prices in the U.S., a desire to ban cultivated meat in Italy, or forcing milk onto kids in lunch programs, alternative protein products face the threat of at best seeing significantly lower consumer adoption or at worst never coming to market at all. A principal example is the attacks on labelling. A recent letter from the U.S. dairy farmers urged the FDA to label animal-free dairy milk as a ‘synthetic whey beverage’. The industry must unite to fight irrational legislation and ensure it is on an even footing with incumbent products. Product and category definitions should be updated to appeal to common sense principles instead of complicating the terminology. If ‘synthetic whey beverage’ is acceptable, as suggested in a recent letter from an incumbent industry group, then perhaps it’s time milk should be termed ‘cow udder extract’?

Misinformation Overload

An onslaught of unbalanced reporting and incomplete information has created doubts in the mind of consumers where there should be none. Alternative proteins can lower greenhouse gases by 30-90% and utilize 72–99% less water than conventional meat11. Yet, the sustainability of the sector continues to be questioned. A recent LCA with questionable assumptions from a prominent university resulted in clickbait headlines about cultivated meat having a 25x higher environmental impact than conventional beef. It was heartening to see alternative protein industry participants put up a joint front to point out the flaws in the analysis. While it will take time for the sector to ramp up its reporting capabilities, it must organize to fight baseless accusations from those with a varied set of agendas that range from promoting animal products to creating clickbait.

Nutrition & Safety Concerns

Alternative protein products and ingredients have faced a barrage of attacks that span nutritional quality, sodium levels, low PDCAAS scores, amino acid composition, and genetically modified products. The term ‘ultra-processed’ or ‘hyper-processed’ is frequently used with plant-based products while incumbents continue to raise questions about the safety of ‘lab-grown meat’. The recent U.S. regulatory approval should help but is unlikely to stop attacks from persisting. Despite the panoply of health concerns with animal products, alternative proteins are routinely put on the defensive. What is hidden from the consumer is the processed nature of animal products, which are often inaccurately billed as ‘natural’. Consumers have little idea of the risks of consuming animal products, or the cruelty underlying their production. This tide must be turned.

Taking Stock

The industry has come a long way. Despite recent headwinds, it is important to recognize that scaling an industry is usually a bumpy road with naysayers doubting progress every step of the way. There is no major innovation that hasn’t faced headwinds from vested interests that seek to protect the status quo, or those that simply feel they can benefit from trumpeting its demise. The hope is for the industry to be able to scale strengths, address weaknesses, leverage opportunities, and tackle threats. With each passing day, we can more vividly see a brighter future ahead for the industry.

From the time Mark Post created a lab-grown burger for $325,000 in 2013, the industry has dreamed of the moment when lab-grown meat would not just be possible, but available to the consumer. That moment is here. The relentless march of technology will enable this offering to become better and cheaper. Along the way, new product formats will emerge and become more widely available. The industry just witnessed an incredible milestone. Significant as it was, what it signals is perhaps even more compelling: the best is still ahead.

EAT Forum Report, Grains of Truth 2022

University of California, Davis

Citibank Research

UN Chronicle

BCG-Blue Horizon, The Untapped Climate Opportunity in Alternative Proteins

Yale Center for Business and the Environment

The New York Times

Barclays Research

First Insight Research

Animal Legal Defense Fund

GFI